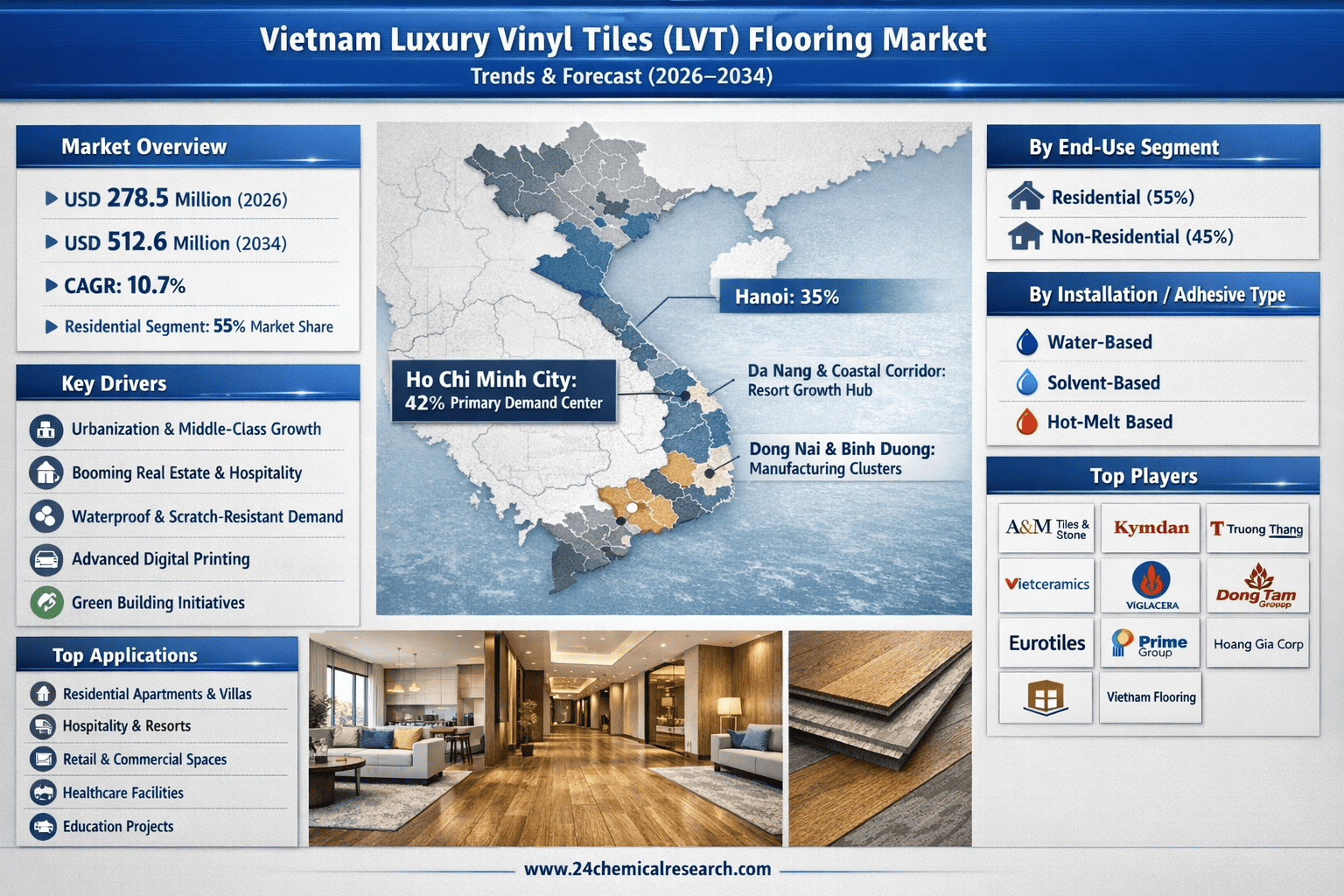

Top 10 Leading Players in Vietnam LVT Flooring Market Driving 10.7% CAGR Growth by 2034

According to 24Chemical Research, Vietnam Luxury Vinyl Tiles (LVT) Flooring Market is projected to grow from USD 278.5 million in 2026 to USD 512.6 million by 2034, registering a strong CAGR of 10.7%. Growth is fueled by Vietnam’s expanding real estate sector, rising middle-class income, and increasing demand for premium yet durable interior finishes.

LVT flooring continues to gain traction for its waterproof, scratch-resistant performance and highly realistic wood and stone aesthetics. Technological advancements, including high-resolution digital printing, now deliver 99.8% design consistency, elevating consumer confidence in vinyl-based flooring.

Regional Growth Highlights

Demand is heavily concentrated in Ho Chi Minh City (42% market share) and Hanoi (35%). Coastal cities such as Da Nang are experiencing rising adoption in hospitality projects, where marine-grade LVT solutions meet tropical climate demands.

Manufacturing investments are expanding in southern provinces, while domestic leaders like Viglacera Corporation strengthen premium product portfolios. International competition intensifies as brands such as LG Hausys expand SPC rigid-core offerings in Vietnam.

Key Growth Drivers

Rapid urban middle-class expansion

Hotel renovation cycles and resort developments

Healthcare and education infrastructure upgrades

Growing DIY adoption via click-lock installation systems

Rising interest in phthalate-free and bio-based formulations

Residential applications account for 55% of demand, while commercial usage—especially hospitality and retail—is growing at double-digit rates. Wood-look designs dominate 62% of consumer preferences, particularly among buyers aged 25–40.

Market Challenges

Volatile PVC resin prices, competitive imports, installation skill shortages, and tightening VOC regulations under QCVN 16:2019 remain key constraints. However, sustainability innovation and Industry 4.0 manufacturing adoption present long-term opportunities.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/280933/vietnam-luxury-vinyl-tiles-flooring-market-2024-2030-136

Get Full Report:

https://www.24chemicalresearch.com/reports/280933/vietnam-luxury-vinyl-tiles-flooring-market-2024-2030-136

About 24Chemical Research

Founded in 2015, 24Chemical Research provides trusted chemical and materials market intelligence to global industry leaders, including 30+ Fortune 500 companies.

According to 24Chemical Research, Vietnam Luxury Vinyl Tiles (LVT) Flooring Market is projected to grow from USD 278.5 million in 2026 to USD 512.6 million by 2034, registering a strong CAGR of 10.7%. Growth is fueled by Vietnam’s expanding real estate sector, rising middle-class income, and increasing demand for premium yet durable interior finishes.

LVT flooring continues to gain traction for its waterproof, scratch-resistant performance and highly realistic wood and stone aesthetics. Technological advancements, including high-resolution digital printing, now deliver 99.8% design consistency, elevating consumer confidence in vinyl-based flooring.

Regional Growth Highlights

Demand is heavily concentrated in Ho Chi Minh City (42% market share) and Hanoi (35%). Coastal cities such as Da Nang are experiencing rising adoption in hospitality projects, where marine-grade LVT solutions meet tropical climate demands.

Manufacturing investments are expanding in southern provinces, while domestic leaders like Viglacera Corporation strengthen premium product portfolios. International competition intensifies as brands such as LG Hausys expand SPC rigid-core offerings in Vietnam.

Key Growth Drivers

Rapid urban middle-class expansion

Hotel renovation cycles and resort developments

Healthcare and education infrastructure upgrades

Growing DIY adoption via click-lock installation systems

Rising interest in phthalate-free and bio-based formulations

Residential applications account for 55% of demand, while commercial usage—especially hospitality and retail—is growing at double-digit rates. Wood-look designs dominate 62% of consumer preferences, particularly among buyers aged 25–40.

Market Challenges

Volatile PVC resin prices, competitive imports, installation skill shortages, and tightening VOC regulations under QCVN 16:2019 remain key constraints. However, sustainability innovation and Industry 4.0 manufacturing adoption present long-term opportunities.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/280933/vietnam-luxury-vinyl-tiles-flooring-market-2024-2030-136

Get Full Report:

https://www.24chemicalresearch.com/reports/280933/vietnam-luxury-vinyl-tiles-flooring-market-2024-2030-136

About 24Chemical Research

Founded in 2015, 24Chemical Research provides trusted chemical and materials market intelligence to global industry leaders, including 30+ Fortune 500 companies.

Top 10 Leading Players in Vietnam LVT Flooring Market Driving 10.7% CAGR Growth by 2034

According to 24Chemical Research, Vietnam Luxury Vinyl Tiles (LVT) Flooring Market is projected to grow from USD 278.5 million in 2026 to USD 512.6 million by 2034, registering a strong CAGR of 10.7%. Growth is fueled by Vietnam’s expanding real estate sector, rising middle-class income, and increasing demand for premium yet durable interior finishes.

LVT flooring continues to gain traction for its waterproof, scratch-resistant performance and highly realistic wood and stone aesthetics. Technological advancements, including high-resolution digital printing, now deliver 99.8% design consistency, elevating consumer confidence in vinyl-based flooring.

Regional Growth Highlights

Demand is heavily concentrated in Ho Chi Minh City (42% market share) and Hanoi (35%). Coastal cities such as Da Nang are experiencing rising adoption in hospitality projects, where marine-grade LVT solutions meet tropical climate demands.

Manufacturing investments are expanding in southern provinces, while domestic leaders like Viglacera Corporation strengthen premium product portfolios. International competition intensifies as brands such as LG Hausys expand SPC rigid-core offerings in Vietnam.

Key Growth Drivers

Rapid urban middle-class expansion

Hotel renovation cycles and resort developments

Healthcare and education infrastructure upgrades

Growing DIY adoption via click-lock installation systems

Rising interest in phthalate-free and bio-based formulations

Residential applications account for 55% of demand, while commercial usage—especially hospitality and retail—is growing at double-digit rates. Wood-look designs dominate 62% of consumer preferences, particularly among buyers aged 25–40.

Market Challenges

Volatile PVC resin prices, competitive imports, installation skill shortages, and tightening VOC regulations under QCVN 16:2019 remain key constraints. However, sustainability innovation and Industry 4.0 manufacturing adoption present long-term opportunities.

📥 Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/280933/vietnam-luxury-vinyl-tiles-flooring-market-2024-2030-136

🔗 Get Full Report:

https://www.24chemicalresearch.com/reports/280933/vietnam-luxury-vinyl-tiles-flooring-market-2024-2030-136

About 24Chemical Research

Founded in 2015, 24Chemical Research provides trusted chemical and materials market intelligence to global industry leaders, including 30+ Fortune 500 companies.

0 Σχόλια

·0 Μοιράστηκε

·66 Views

·0 Προεπισκόπηση