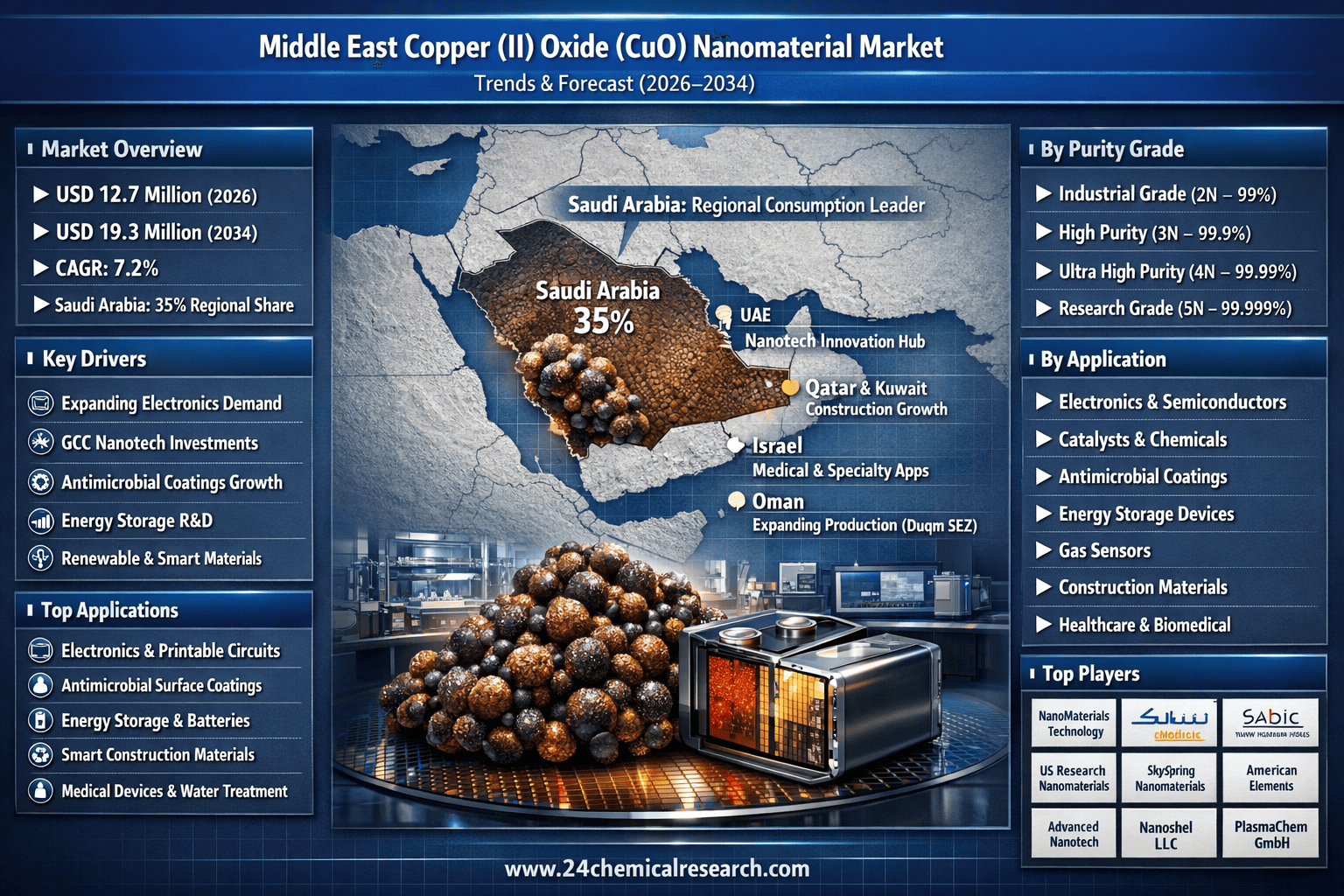

Why Is Middle East CuO Nanomaterial Market Expected to Grow at a 7.2% CAGR Through 2034?

According to 24Chemical Research, Middle East Copper (II) Oxide (CuO) Nanomaterial Market is projected to grow from USD 12.7 million in 2026 to USD 19.3 million by 2034, registering a CAGR of 7.2%. Growth is fueled by expanding applications in electronics, antimicrobial coatings, and energy storage, alongside rising nanotechnology investments across GCC economies.

CuO nanomaterials are increasingly valued for their electrical conductivity, thermal stability, and antimicrobial efficiency. Regional R&D spending in nanotechnology rose 18% in 2023, strengthening local production capabilities and accelerating commercialization.

Regional Leadership & Capacity Expansion

Saudi Arabia leads regional demand with 35% market share, supported by industrialization initiatives under Vision 2030. The United Arab Emirates follows closely, leveraging advanced research ecosystems and free zones to position itself as a nanotech hub. Institutions such as Masdar Institute have pioneered conductive nanocomposite research using CuO materials.

Qatar and Kuwait are driving adoption in construction and antimicrobial coatings, while Israel dominates high-value applications in medical devices and water treatment. Regional production capacity reached 175 metric tons in 2023, with expansion underway in Oman’s Duqm Special Economic Zone.

Key Growth Drivers

Electronics & semiconductor applications (40% demand share)

Antimicrobial coatings growing at 10% annually

Energy storage R&D projects expanding by 30%

Renewable energy ambitions across GCC nations

Emerging smart textile applications

CuO’s photothermal efficiency in solar cells and its p-type semiconductor properties enhance its role in next-generation technologies.

Challenges

Price volatility in copper feedstock, regulatory fragmentation across jurisdictions, and nanoparticle dispersion limitations remain constraints. However, green synthesis methods—growing 20% in 2023—signal a shift toward sustainable production models.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/280714/middle-east-copper-oxide-nanomaterial-market-2024-2030-671

Get Full Report:

https://www.24chemicalresearch.com/reports/280714/middle-east-copper-oxide-nanomaterial-market-2024-2030-671

About 24Chemical Research

Founded in 2015, 24Chemical Research delivers data-driven chemical and materials market intelligence, serving 30+ Fortune 500 companies globally.

According to 24Chemical Research, Middle East Copper (II) Oxide (CuO) Nanomaterial Market is projected to grow from USD 12.7 million in 2026 to USD 19.3 million by 2034, registering a CAGR of 7.2%. Growth is fueled by expanding applications in electronics, antimicrobial coatings, and energy storage, alongside rising nanotechnology investments across GCC economies.

CuO nanomaterials are increasingly valued for their electrical conductivity, thermal stability, and antimicrobial efficiency. Regional R&D spending in nanotechnology rose 18% in 2023, strengthening local production capabilities and accelerating commercialization.

Regional Leadership & Capacity Expansion

Saudi Arabia leads regional demand with 35% market share, supported by industrialization initiatives under Vision 2030. The United Arab Emirates follows closely, leveraging advanced research ecosystems and free zones to position itself as a nanotech hub. Institutions such as Masdar Institute have pioneered conductive nanocomposite research using CuO materials.

Qatar and Kuwait are driving adoption in construction and antimicrobial coatings, while Israel dominates high-value applications in medical devices and water treatment. Regional production capacity reached 175 metric tons in 2023, with expansion underway in Oman’s Duqm Special Economic Zone.

Key Growth Drivers

Electronics & semiconductor applications (40% demand share)

Antimicrobial coatings growing at 10% annually

Energy storage R&D projects expanding by 30%

Renewable energy ambitions across GCC nations

Emerging smart textile applications

CuO’s photothermal efficiency in solar cells and its p-type semiconductor properties enhance its role in next-generation technologies.

Challenges

Price volatility in copper feedstock, regulatory fragmentation across jurisdictions, and nanoparticle dispersion limitations remain constraints. However, green synthesis methods—growing 20% in 2023—signal a shift toward sustainable production models.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/280714/middle-east-copper-oxide-nanomaterial-market-2024-2030-671

Get Full Report:

https://www.24chemicalresearch.com/reports/280714/middle-east-copper-oxide-nanomaterial-market-2024-2030-671

About 24Chemical Research

Founded in 2015, 24Chemical Research delivers data-driven chemical and materials market intelligence, serving 30+ Fortune 500 companies globally.

Why Is Middle East CuO Nanomaterial Market Expected to Grow at a 7.2% CAGR Through 2034?

According to 24Chemical Research, Middle East Copper (II) Oxide (CuO) Nanomaterial Market is projected to grow from USD 12.7 million in 2026 to USD 19.3 million by 2034, registering a CAGR of 7.2%. Growth is fueled by expanding applications in electronics, antimicrobial coatings, and energy storage, alongside rising nanotechnology investments across GCC economies.

CuO nanomaterials are increasingly valued for their electrical conductivity, thermal stability, and antimicrobial efficiency. Regional R&D spending in nanotechnology rose 18% in 2023, strengthening local production capabilities and accelerating commercialization.

Regional Leadership & Capacity Expansion

Saudi Arabia leads regional demand with 35% market share, supported by industrialization initiatives under Vision 2030. The United Arab Emirates follows closely, leveraging advanced research ecosystems and free zones to position itself as a nanotech hub. Institutions such as Masdar Institute have pioneered conductive nanocomposite research using CuO materials.

Qatar and Kuwait are driving adoption in construction and antimicrobial coatings, while Israel dominates high-value applications in medical devices and water treatment. Regional production capacity reached 175 metric tons in 2023, with expansion underway in Oman’s Duqm Special Economic Zone.

Key Growth Drivers

Electronics & semiconductor applications (40% demand share)

Antimicrobial coatings growing at 10% annually

Energy storage R&D projects expanding by 30%

Renewable energy ambitions across GCC nations

Emerging smart textile applications

CuO’s photothermal efficiency in solar cells and its p-type semiconductor properties enhance its role in next-generation technologies.

Challenges

Price volatility in copper feedstock, regulatory fragmentation across jurisdictions, and nanoparticle dispersion limitations remain constraints. However, green synthesis methods—growing 20% in 2023—signal a shift toward sustainable production models.

📥 Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/280714/middle-east-copper-oxide-nanomaterial-market-2024-2030-671

🔗 Get Full Report:

https://www.24chemicalresearch.com/reports/280714/middle-east-copper-oxide-nanomaterial-market-2024-2030-671

About 24Chemical Research

Founded in 2015, 24Chemical Research delivers data-driven chemical and materials market intelligence, serving 30+ Fortune 500 companies globally.

0 Commenti

·0 condivisioni

·89 Views

·0 Anteprima