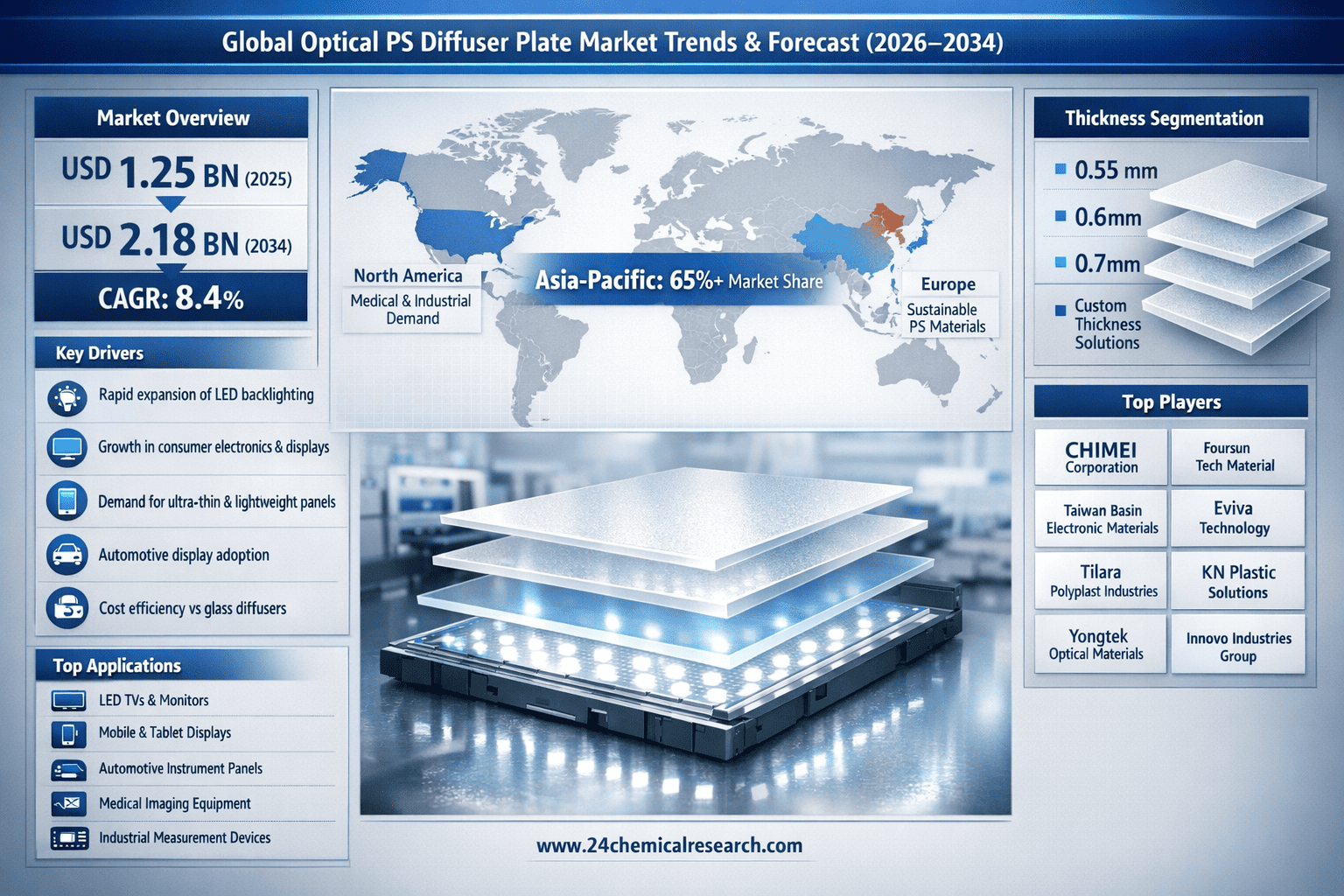

Why Is Global Optical PS Diffuser Plate Market Expected to Grow at an 8.4% CAGR from 2026 to 2034?

According to 24Chemical Research, Global Optical PS Diffuser Plate Market was valued at USD 1.25 billion in 2025 and is projected to reach approximately USD 2.18 billion by 2034, expanding at a robust CAGR of 8.4% during the forecast period. This accelerated growth is primarily driven by the rapid expansion of LED backlighting applications, rising demand for high-performance consumer electronics, and increasing adoption of advanced display technologies worldwide.

Optical PS (Polystyrene) diffuser plates are critical components in liquid crystal display (LCD) systems, where they ensure uniform light distribution from LED sources while maintaining high optical clarity. Their lightweight structure, cost efficiency, and design flexibility make them a preferred alternative to glass, particularly in mobile devices, ultra-thin TVs, and compact electronic displays.

Asia-Pacific Leads Global Production and Consumption

The Asia-Pacific region accounts for over 65% of global production capacity, with China serving as the manufacturing hub and largest consumer. The region’s dominance is supported by vertically integrated display supply chains, proximity to major electronics assemblers in South Korea, Japan, and Taiwan, and strong government incentives encouraging domestic display component manufacturing. Continuous R&D investments in next-generation display materials further reinforce regional leadership.

In contrast, North America and Europe focus on high-performance and specialty diffuser plates, particularly for medical imaging, industrial inspection, and automotive displays, where optical precision and durability are critical. Increasing environmental regulations in these regions are also accelerating demand for recyclable and sustainable PS materials.

Key Growth Drivers Fueling Market Expansion

Several converging trends are driving sustained market growth:

Large-format digital signage and commercial displays, which require advanced diffusion solutions to eliminate light hotspots

Gaming monitors and high-refresh-rate displays, where precise light management enhances visual performance

Automotive display systems, including instrument clusters and infotainment panels, demanding thermal stability and optical consistency

Emerging opportunities are also taking shape in micro-LED displays, smart home devices, and interactive control panels. Additionally, the medical sector presents untapped potential for antimicrobial optical PS diffuser plates in diagnostic and hospital equipment.

Challenges and Market Constraints

Despite strong momentum, the market faces several challenges. Volatility in styrene monomer prices directly affects manufacturing costs, while competition from PMMA alternatives—known for higher optical clarity—remains intense. Environmental regulations related to PS recycling and waste management are prompting manufacturers to invest in closed-loop production systems.

Technologically, suppliers must continuously balance diffusion efficiency with minimal light loss, especially as global energy efficiency standards for displays become more stringent.

Competitive Landscape and Market Segmentation

The market features a mix of global chemical majors and regional specialists, including CHIMEI Corporation, Sumitomo Chemical, Asahi Kasei, LG Chem, Toray Industries, Teijin Limited, and a growing number of Asia-based material innovators. Competition centers on optical performance, thickness customization, cost control, and supply reliability.

Segment-wise growth is strongest in custom thickness solutions and applications such as LED TVs, automotive displays, medical imaging equipment, and industrial measurement devices.

Outlook Through 2034

With display technologies evolving rapidly and demand rising across consumer, automotive, and medical sectors, the Optical PS Diffuser Plate market is positioned for sustained high-growth expansion. Manufacturers investing in advanced diffusion technology, sustainability initiatives, and regional supply resilience are expected to gain a competitive edge.

Get Full Report:

https://www.24chemicalresearch.com/reports/272996/global-optical-ps-diffuser-plate-market-2024-2030-659

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/272996/global-optical-ps-diffuser-plate-market-2024-2030-659

About 24Chemical Research

Founded in 2015, 24Chemical Research provides data-driven chemical and materials market intelligence to 30+ Fortune 500 companies, delivering plant-level capacity tracking, real-time price monitoring, and techno-economic feasibility studies.

Why Is Global Optical PS Diffuser Plate Market Expected to Grow at an 8.4% CAGR from 2026 to 2034?

According to 24Chemical Research, Global Optical PS Diffuser Plate Market was valued at USD 1.25 billion in 2025 and is projected to reach approximately USD 2.18 billion by 2034, expanding at a robust CAGR of 8.4% during the forecast period. This accelerated growth is primarily driven by the rapid expansion of LED backlighting applications, rising demand for high-performance consumer electronics, and increasing adoption of advanced display technologies worldwide.

Optical PS (Polystyrene) diffuser plates are critical components in liquid crystal display (LCD) systems, where they ensure uniform light distribution from LED sources while maintaining high optical clarity. Their lightweight structure, cost efficiency, and design flexibility make them a preferred alternative to glass, particularly in mobile devices, ultra-thin TVs, and compact electronic displays.

Asia-Pacific Leads Global Production and Consumption

The Asia-Pacific region accounts for over 65% of global production capacity, with China serving as the manufacturing hub and largest consumer. The region’s dominance is supported by vertically integrated display supply chains, proximity to major electronics assemblers in South Korea, Japan, and Taiwan, and strong government incentives encouraging domestic display component manufacturing. Continuous R&D investments in next-generation display materials further reinforce regional leadership.

In contrast, North America and Europe focus on high-performance and specialty diffuser plates, particularly for medical imaging, industrial inspection, and automotive displays, where optical precision and durability are critical. Increasing environmental regulations in these regions are also accelerating demand for recyclable and sustainable PS materials.

Key Growth Drivers Fueling Market Expansion

Several converging trends are driving sustained market growth:

Large-format digital signage and commercial displays, which require advanced diffusion solutions to eliminate light hotspots

Gaming monitors and high-refresh-rate displays, where precise light management enhances visual performance

Automotive display systems, including instrument clusters and infotainment panels, demanding thermal stability and optical consistency

Emerging opportunities are also taking shape in micro-LED displays, smart home devices, and interactive control panels. Additionally, the medical sector presents untapped potential for antimicrobial optical PS diffuser plates in diagnostic and hospital equipment.

Challenges and Market Constraints

Despite strong momentum, the market faces several challenges. Volatility in styrene monomer prices directly affects manufacturing costs, while competition from PMMA alternatives—known for higher optical clarity—remains intense. Environmental regulations related to PS recycling and waste management are prompting manufacturers to invest in closed-loop production systems.

Technologically, suppliers must continuously balance diffusion efficiency with minimal light loss, especially as global energy efficiency standards for displays become more stringent.

Competitive Landscape and Market Segmentation

The market features a mix of global chemical majors and regional specialists, including CHIMEI Corporation, Sumitomo Chemical, Asahi Kasei, LG Chem, Toray Industries, Teijin Limited, and a growing number of Asia-based material innovators. Competition centers on optical performance, thickness customization, cost control, and supply reliability.

Segment-wise growth is strongest in custom thickness solutions and applications such as LED TVs, automotive displays, medical imaging equipment, and industrial measurement devices.

Outlook Through 2034

With display technologies evolving rapidly and demand rising across consumer, automotive, and medical sectors, the Optical PS Diffuser Plate market is positioned for sustained high-growth expansion. Manufacturers investing in advanced diffusion technology, sustainability initiatives, and regional supply resilience are expected to gain a competitive edge.

🔹 Get Full Report:

https://www.24chemicalresearch.com/reports/272996/global-optical-ps-diffuser-plate-market-2024-2030-659

🔹 Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/272996/global-optical-ps-diffuser-plate-market-2024-2030-659

About 24Chemical Research

Founded in 2015, 24Chemical Research provides data-driven chemical and materials market intelligence to 30+ Fortune 500 companies, delivering plant-level capacity tracking, real-time price monitoring, and techno-economic feasibility studies.