Advanced Driver Assistance Systems Market Drivers, Challenges, and Forecast 2032

The Advanced Driver Assistance Systems Market is experiencing unprecedented growth as automotive technologies evolve toward autonomous and semi-autonomous mobility. Valued at US$ 33,989.89 million in 2024, the market is projected to expand at a robust CAGR of 12.5% from 2025 to 2032. The increasing demand for vehicle safety, accident prevention, and smart mobility solutions is driving adoption of ADAS technologies across passenger cars, commercial vehicles, and electric vehicle segments worldwide. Advanced sensors, integrated software, and intelligent hardware platforms are becoming critical enablers of real-time vehicle perception, decision-making, and automated response functionalities.

Market Highlights

• Dominance of Passenger Cars and Expanding Commercial Vehicle Adoption

Passenger cars represent the largest segment, propelled by increasing consumer demand for driver assistance technologies such as lane-keeping systems, adaptive cruise control, and automated emergency braking. Simultaneously, commercial vehicles including buses, trucks, and light commercial vehicles are increasingly equipped with ADAS for fleet safety, regulatory compliance, and operational efficiency.

• System Type Innovations Driving Growth

ADAS technologies encompass a variety of system types, including radar, LiDAR, camera-based systems, ultrasonic sensors, and infrared detection platforms. Integration of these systems enhances vehicle perception and allows advanced functionalities such as blind-spot monitoring, collision avoidance, and parking assistance. The growing sophistication of sensor fusion technology is enabling higher accuracy and reliability of autonomous decision-making.

• Electric Vehicle Integration

With the rise of electric vehicles (EVs), ADAS adoption is accelerating. EV manufacturers are increasingly embedding driver assistance technologies to improve safety and optimize energy consumption through smart navigation, predictive braking, and automated lane guidance. The synergy between EVs and ADAS is fueling demand for intelligent software and sensor-based hardware solutions tailored for battery-powered mobility.

• Autonomy Levels and Software Advancements

Market expansion is strongly influenced by the increasing development of vehicles with varying autonomy levels, from Level 1 driver assistance to Level 4 highly automated vehicles. Advanced software offerings, including AI-powered perception algorithms, machine learning-enabled predictive analytics, and over-the-air updates, are enhancing system adaptability and real-time decision-making capabilities.

• Hardware Innovation Enhancing System Performance

Hardware offerings such as high-precision sensors, semiconductor chips, embedded processors, and connectivity modules are critical for ADAS functionality. Technological advancements in radar resolution, LiDAR miniaturization, and camera optics are enabling improved situational awareness, obstacle detection, and response speed.

End-User & Regional Insights

Automobile manufacturers, component suppliers, and technology integrators are the primary adopters of ADAS. OEMs increasingly collaborate with semiconductor companies and software developers to integrate complete ADAS solutions into vehicles. Fleet operators in commercial segments are leveraging ADAS for driver safety, compliance, and efficiency gains.

Regionally, North America leads the market due to early adoption of advanced automotive safety regulations, high consumer awareness, and substantial R&D investments. Europe follows closely, driven by stringent safety mandates and regulatory support for semi-autonomous vehicles. Asia-Pacific is emerging as a high-growth region, fueled by rapid vehicle production, increasing government initiatives for road safety, and rising EV penetration.

Competitive Landscape – Strategic Developments

The ADAS market is highly competitive and characterized by continuous innovation, strategic partnerships, and mergers and acquisitions. Leading companies are focusing on integrated ADAS platforms that combine advanced software, sensing, and connectivity solutions. Key players include Renesas Electronics Corporation, Denso Corporation, Valeo SA, Magna International Inc., Continental AG, Panasonic Holdings Corporation, and Texas Instruments Incorporated. These companies invest heavily in R&D to enhance system reliability, improve automation capabilities, and maintain technological leadership. Collaborative initiatives between automakers and technology providers are also accelerating the deployment of ADAS features across multiple vehicle segments.

Growth Drivers & Market Dynamics

• Rising Safety Concerns and Regulatory Compliance

Stringent global safety regulations and increasing government mandates for collision avoidance systems are driving the adoption of ADAS technologies. Accident prevention and reduction of traffic-related fatalities are critical factors promoting system integration.

• Expansion of Electric & Connected Vehicles

The proliferation of electric vehicles and connected car platforms is accelerating demand for intelligent driver assistance systems. Integration of ADAS ensures compatibility with EV architecture and enables enhanced energy management, route optimization, and predictive maintenance.

• Technological Integration with AI & Machine Learning

Artificial intelligence and machine learning algorithms improve situational awareness, predictive analytics, and adaptive decision-making. Continuous software updates enable vehicles to learn and respond to dynamic road environments, enhancing both safety and convenience.

• Consumer Awareness and Feature Demand

Increasing consumer preference for vehicles equipped with lane departure warning, adaptive cruise control, automatic emergency braking, and parking assistance is driving market growth. Awareness campaigns and rising expectations for premium vehicle safety features further strengthen adoption.

Challenges & Future Outlook

Key challenges include high system development costs, complex integration requirements, and cybersecurity risks associated with connected vehicles. Additionally, variability in regional regulatory frameworks and technological standardization may impact adoption rates. Despite these hurdles, continued investments in sensor technologies, AI-driven software, and high-performance hardware are expected to accelerate innovation and market penetration.

Looking forward, the convergence of ADAS with autonomous driving, vehicle-to-everything (V2X) communication, and electric mobility is anticipated to reshape global automotive ecosystems. Collaborative ventures between automotive OEMs, semiconductor manufacturers, and software developers will remain pivotal in delivering highly sophisticated, safe, and scalable driver assistance solutions.

For detailed segmentation, regional forecasts, and in-depth market insights, stakeholders can explore the complete report and request additional data via the Advanced Driver Assistance Systems Market.

Browse more Report:

Industrial Discrete Semiconductor Market

Electronic Materials and Chemicals Market

E-Beam Wafer Inspection System Market

Categorías

Read More

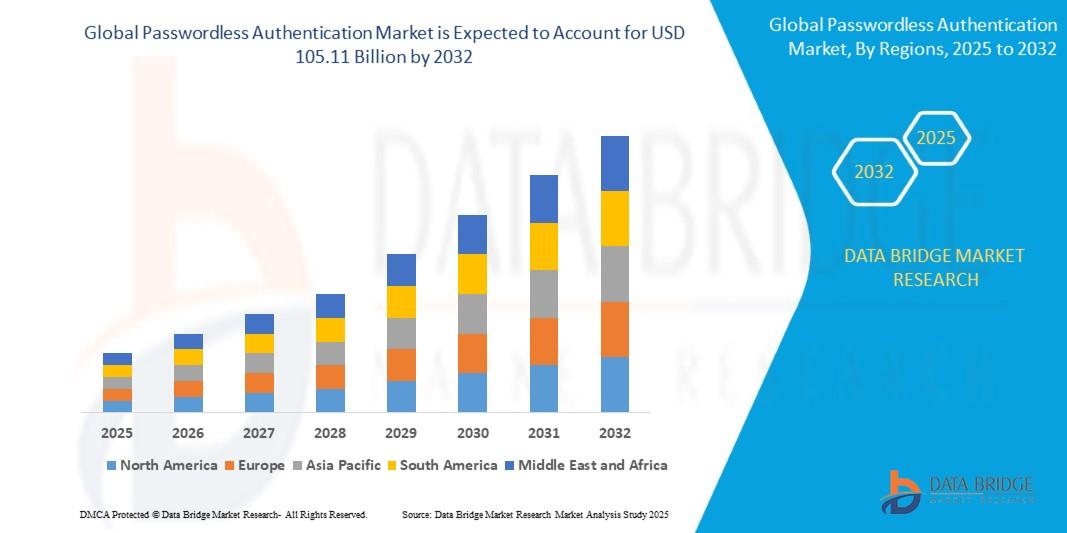

"Market Trends Shaping Executive Summary Passwordless Authentication Market Size and Share CAGR Value The global passwordless authentication market size was valued at USD 16.33 billion in 2024 and is expected to reach USD 105.11 billion by 2032, at a CAGR of 26.20% during the forecast period An excellent Passwordless Authentication Market report gives out...

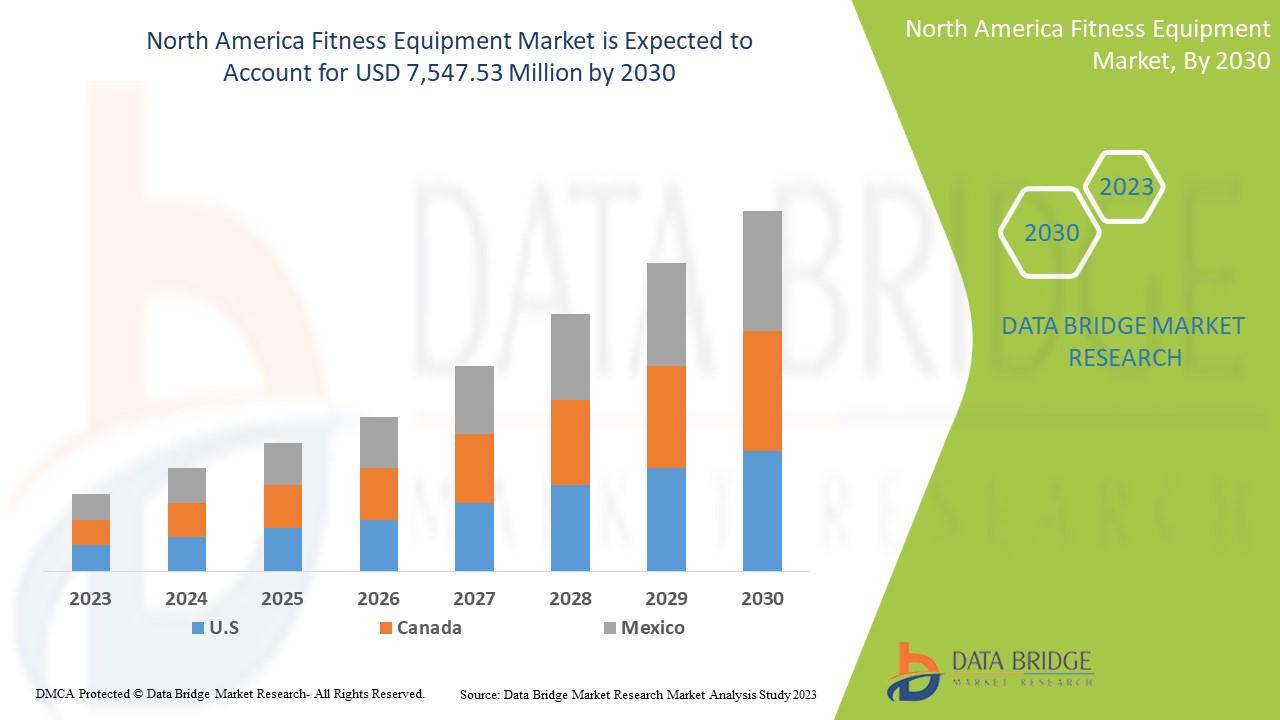

Executive Summary North America Fitness Equipment Market: Size, Share, and Forecast to 2030 CAGR Value Data Bridge Market Research analyzes that the North America fitness equipment market is expected to reach the value of USD 7,547.53 million by 2030, at a CAGR of 7.3% during the forecast period. This market report also covers pricing analysis, patent analysis, and technological...

Introduction The Olive Oil Market is one of the most dynamic segments within the global food and beverage industry. Olive oil, extracted from the fruit of the olive tree (Olea europaea), has been a staple of Mediterranean cuisine for centuries. Today, it is recognized globally not only for its culinary versatility but also for its numerous health benefits. Known for being rich in...

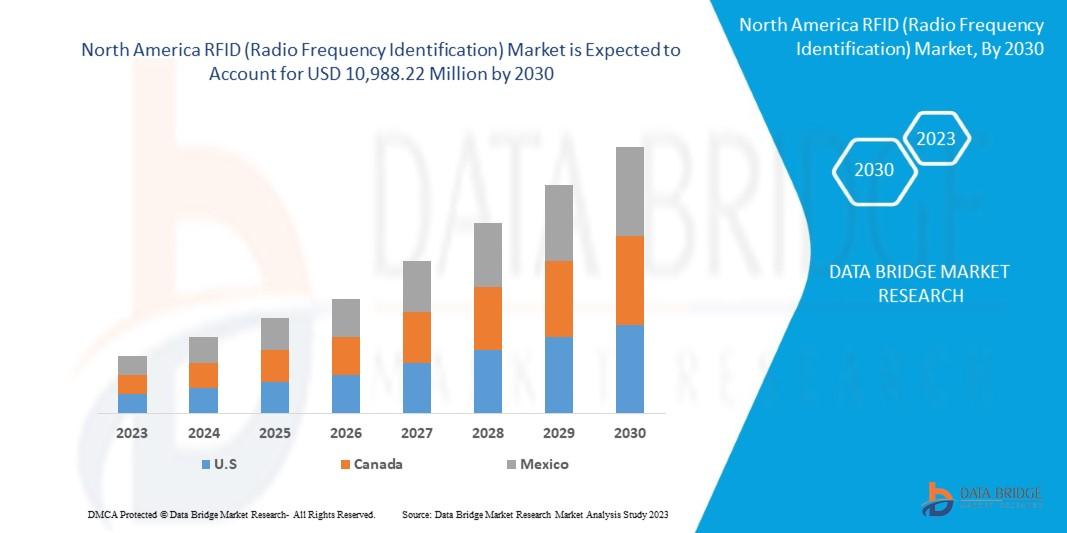

Introduction The North America RFID (Radio Frequency Identification) Market represents a major segment of the global identification and tracking technology industry. RFID uses electromagnetic fields to identify and track tags attached to objects, allowing seamless data collection and asset management. It has become a cornerstone of automation, logistics, retail, and industrial...

Analyse concurrentielle du résumé exécutif : taille et part de marché du papier kraft Le marché mondial du papier kraft était évalué à 19,44 milliards USD en 2024 et devrait atteindre 26,81 milliards USD d'ici 2032. Au cours de la période de prévision de 2025 à...