Beyond the Battery: The Global Evolution of the Fuel Cell Market

The global quest for energy security and decarbonization has propelled the Fuel Cell Market into a new era of commercial maturity. As of 2026, the industry is no longer characterized by experimental prototypes but by the mass production of high-efficiency systems that turn chemical energy directly into electricity. This transition is being driven by the limitations of traditional battery storage in heavy-duty and long-duration applications. While batteries dominate the light passenger vehicle segment, fuel cells have carved out a dominant position in sectors that require rapid refueling, long ranges, and high power density, such as international shipping, transcontinental trucking, and mission-critical backup power for the digital economy.

Technological Pillars: PEM and Solid Oxide Dominance

The current market is bifurcated between two primary technologies, each serving distinct industrial needs. Proton Exchange Membrane Fuel Cells (PEMFC) remain the most widely deployed technology, particularly in the transportation sector. Their low operating temperatures and quick start-up times make them the gold standard for fuel cell electric vehicles (FCEVs) and material handling equipment like forklifts. By 2026, improvements in membrane durability and a significant reduction in the use of platinum catalysts have made PEM systems more cost-competitive with traditional diesel engines.

Conversely, Solid Oxide Fuel Cells (SOFC) are seeing an explosive growth rate in the stationary power segment. Operating at much higher temperatures, SOFCs are highly prized for their fuel flexibility—capable of running on hydrogen, natural gas, or even ammonia—and their extreme efficiency when used in Combined Heat and Power (CHP) configurations. Large-scale data centers and hospitals are increasingly adopting SOFC systems to ensure grid resilience and provide a steady baseload of clean energy that functions independently of the primary electrical grid.

Market Drivers: Policy, Infrastructure, and Resilience

The acceleration of the fuel cell industry is largely underpinned by a favorable global regulatory environment. In the United States, the continued impact of the Inflation Reduction Act has provided the long-term tax certainty needed for fleet operators to switch to hydrogen. In Europe, the "Fit for 55" package has mandated the installation of hydrogen refueling stations every 200 kilometers along major transport corridors, effectively solving the "chicken-and-egg" problem that previously hindered vehicle adoption.

Furthermore, the rise of "Hydrogen Hubs" has localized the supply chain. By co-locating hydrogen production with industrial end-users, these hubs have drastically reduced the costs associated with hydrogen compression and transport. This integrated approach has allowed the market to scale vertically, with major players now offering "Hydrogen-as-a-Service" models, where customers pay for the power generated rather than the upfront cost of the fuel cell hardware.

Regional Leadership and Competitive Landscape

Geographically, Asia-Pacific remains the largest and fastest-growing market. Led by Japan’s "Hydrogen Society" vision and South Korea’s aggressive subsidies for fuel cell power plants, the region has established a formidable lead in manufacturing and deployment. China has also emerged as a massive player, specifically targeting the commercial bus and logistics truck markets to improve urban air quality.

North America and Europe are following closely, with a strategic focus on high-value applications. The North American market is currently dominated by stationary power for industrial facilities and the rapid electrification of warehouse logistics. In Europe, the focus is squarely on the maritime and heavy-rail sectors, where fuel cells are being integrated into massive container ships and regional trains to meet stringent new carbon emission standards for 2026.

Challenges and the Path Ahead

Despite the record-breaking growth, the market faces persistent hurdles. The high capital expenditure for fuel cell stacks remains a barrier for small and medium-sized enterprises. While costs are falling, the industry is still working toward the economies of scale required to achieve true price parity with internal combustion engines. Additionally, the global supply of green hydrogen—produced via renewable-powered electrolysis—must continue to expand to ensure that fuel cells provide the maximum environmental benefit.

As we look toward the end of the decade, the focus is shifting toward "circularity." Manufacturers are developing advanced recycling programs to recover precious metals from spent fuel cell stacks, further reducing environmental impact and stabilizing material costs. With the continued integration of Artificial Intelligence to optimize stack performance and the expansion of the global hydrogen pipeline network, the fuel cell market is set to remain a vital component of the 21st-century energy mix.

Frequently Asked Questions

What are the main advantages of fuel cells over batteries? While batteries are excellent for light vehicles, fuel cells offer much faster refueling times (similar to diesel) and much higher energy density. This makes them more suitable for heavy-duty applications like long-haul trucks, ships, and trains, where the weight and charging time of large battery packs would be impractical.

Which industries are currently the biggest users of fuel cell technology? The transportation sector is the largest user, particularly for commercial fleets, buses, and forklifts. However, the stationary power sector is growing rapidly, with data centers and telecommunications hubs using fuel cells for reliable, clean backup power.

What is the difference between PEM and Solid Oxide fuel cells? PEM (Proton Exchange Membrane) fuel cells operate at lower temperatures and are best for mobile applications like cars and trucks. Solid Oxide (SOFC) fuel cells operate at high temperatures, are more efficient for continuous power generation, and can use various fuels like natural gas or ammonia in addition to hydrogen.

More Trending Reports on Energy & Power by Market Research Future

Variable Frequency Drive Market Size

Категории

Больше

Executive Summary Fire Protection System Market: Growth Trends and Share Breakdown The global fire protection system market size was valued at USD 81.22 billion in 2024 and is projected to reach USD 150.11 billion by 2032, with a CAGR of 7.98% during the forecast period of 2025 to 2032. The Fire Protection System Market report has been formed with the appropriate expertise's that utilize...

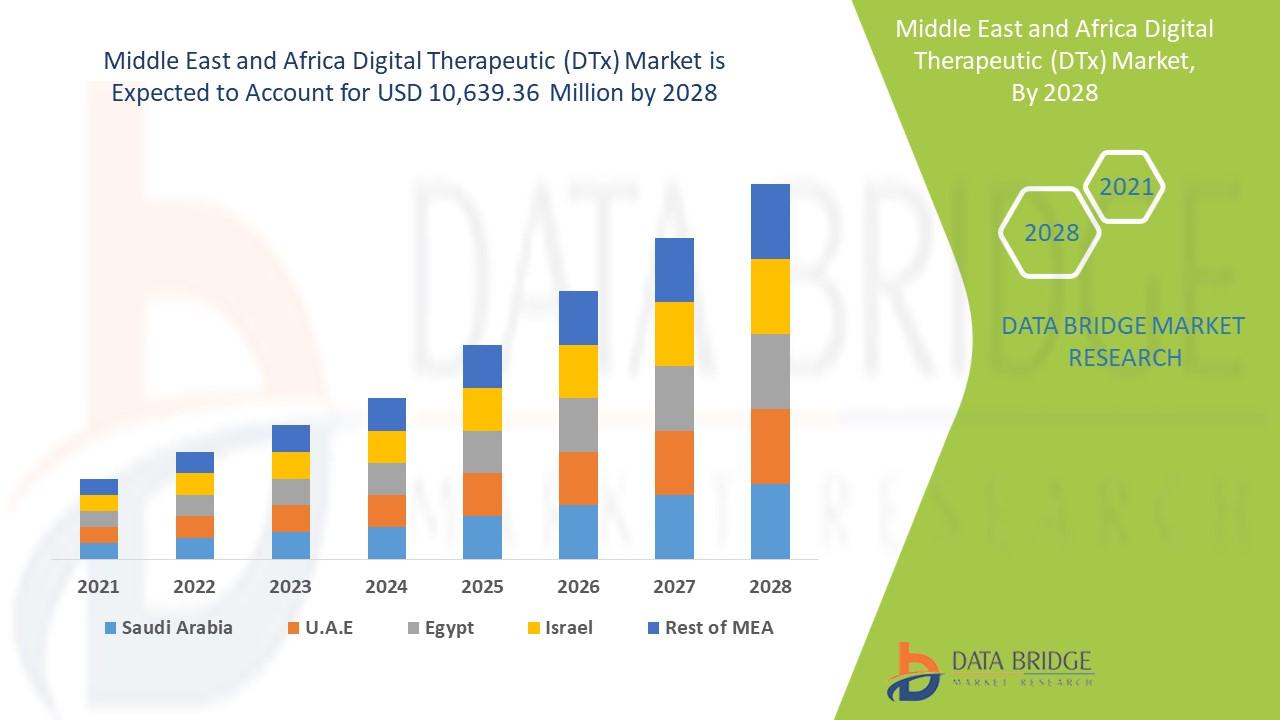

What’s Fueling Executive Summary Middle East and Africa Digital Therapeutic (DTx) Market Size and Share Growth CAGR Value Data Bridge Market Research analyses that the market is growing with a CAGR of 23.4% in the forecast period of 2021 to 2028 and is expected to reach USD 10,639.36 million by 2028. An influential Middle East and Africa Digital Therapeutic (DTx) Market document...

According to the research report, the global Baby Sleeping Bag market was valued at USD 323.41 million in 2022 and is expected to reach USD 519.33 million by 2032, to grow at a CAGR of 4.9% during the forecast period. The global baby sleeping bags market is witnessing strong growth as parents worldwide increasingly prioritize safe, comfortable, and convenient sleep solutions for their...

The projected future worth of a market is a direct measure of its economic significance, and the anticipated Geospatial Market Value of USD 274.41 million by 2035 is a clear indicator of its growing importance as a critical enterprise technology. This valuation, which is set to be achieved through a period of strong growth at a 9.12% CAGR from 2025, represents the total global...

Global Demand Outlook for Executive Summary Argentina Menopause Drugs Market Size and Share Argentina menopause drugs market is expected to gain market growth in the forecast period of 2022 to 2029. Data Bridge Market Research analyses that the market is growing with a CAGR of 4.6% in the forecast period of 2022 to 2029 and is expected to reach USD 50.80 million by 2029 from USD 35.65...