An Industry of Flows: The Structure of the Global Remittance Industry

To fully comprehend the massive global movement of personal funds, it is essential to understand the intricate structure of the Remittance Industry. This is not a simple industry of banks; it is a complex, multi-layered ecosystem where traditional money transfer operators, modern fintech companies, correspondent banks, and local payout partners all play a critical and often interdependent role. This industry is at the intersection of international finance, retail services, and technology. The interactions between these diverse players are what create the global network that allows a construction worker in Dubai to send money that can be picked up as cash by their family in a small village in the Philippines within minutes. Understanding the different layers and players within this industrial structure is key to appreciating the operational complexity and the competitive dynamics of this vital global service.

At the front end of the industry, interacting directly with the senders, are the money transfer companies. This group is broadly divided into two categories. The first is the incumbent, traditional Money Transfer Operators (MTOs), dominated by Western Union and MoneyGram. Their primary asset is their vast global network of physical agent locations, which provides a trusted and accessible cash-in point for millions of migrants. The second, and rapidly growing, category is the digital-first remittance companies, such as Wise, Remitly, and WorldRemit. These fintech players operate primarily through mobile apps and websites, attracting customers with their lower fees, better exchange rates, and superior user experience. This battle between the physical-first incumbents and the digital-first disruptors is the defining competitive dynamic of the industry today.

The middle of the industry structure is the complex and often invisible "plumbing" of cross-border payments. This is where the money is actually moved from one country to another. For traditional players, this often involves a network of correspondent banking relationships. The sending agent's bank in one country has a relationship with a partner bank in the receiving country, and the funds are settled between these banks. Digital players often use more innovative methods to reduce costs, such as pre-funding accounts in different countries and matching local transfers to avoid actual cross-border settlements. The Remittance Market is Expected to Grow a Valuation of USD 85.44 Billion By 2035, Growing at a CAGR of 3.80% During the Forecast Period 2025 - 2035. This part of the industry is also subject to intense regulatory oversight, with all players needing to adhere to strict anti-money laundering (AML) and know-your-customer (KYC) rules.

At the other end of the transaction is the crucial "last-mile" payout network. This is the infrastructure that allows the recipient to actually access the funds in their local currency. For traditional MTOs, this is their network of cash pick-up agent locations. For digital players, the payout network is more diverse. It includes partnerships with local banks to enable direct bank deposits. Crucially, it also includes partnerships with local mobile money operators, particularly in Africa and Asia. This allows funds to be sent directly to a recipient's mobile money wallet, which is often more convenient and accessible than a bank account. A strong and diverse payout network is a key competitive advantage, as it determines the convenience and accessibility of the service for the recipient, which is a major factor in the sender's choice of provider.

Explore More Like This in Our Regional Reports:

Japan Artificial Intelligence (AI) Market Size

South Korea Artificial Intelligence (AI) Market Size

Κατηγορίες

Διαβάζω περισσότερα

Pancreatic cancer remains one of the most aggressive and difficult-to-treat cancers worldwide. According to the World Cancer Research Fund International, it is among the most common cancers globally, with treatment options largely dependent on the stage and tumor location at the time of diagnosis. Owing to its late detection and poor prognosis, major pharmaceutical companies and research...

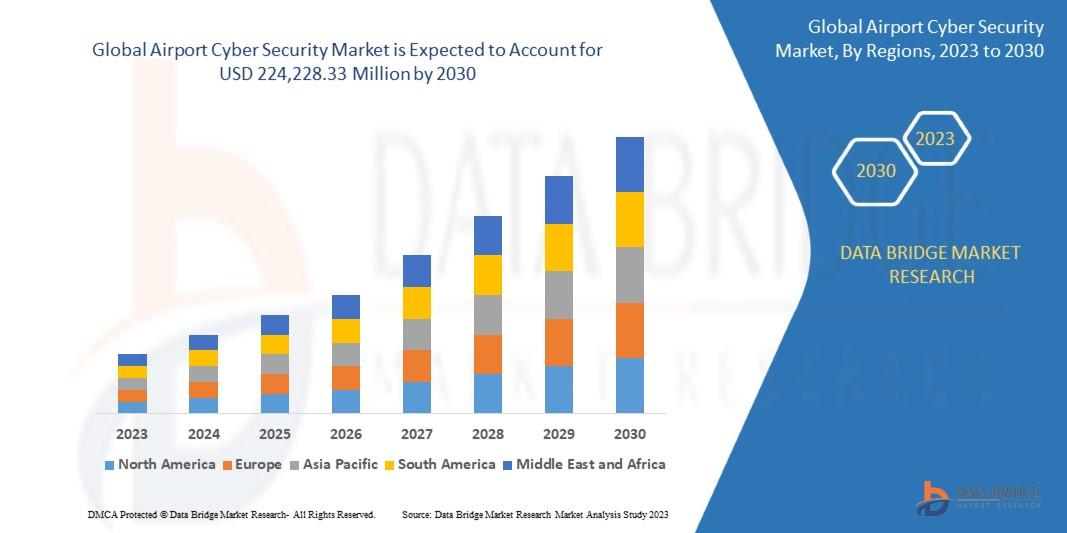

Introduction The Airport Cyber Security Market refers to technologies, systems, and services designed to protect airport digital infrastructure, communication networks, and operational systems from cyber threats. With increasing digitization of airport operations—ranging from passenger data management to air traffic control—cybersecurity has become a critical component of...

The global lithium drug market size was valued at USD 148.29 million in 2024 and is expected to reach USD 215.77 million by 2032, at a CAGR of 4.30% during the forecast period. The global business landscape is undergoing a transformation, with industries increasingly leaning on deep research and actionable insights to make strategic decisions. One segment seeing...

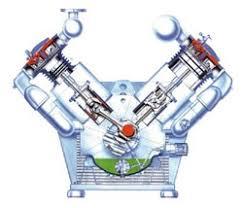

Introduction The V Shaped Compressors Market is experiencing steady growth as industries worldwide adopt compact, efficient, and high-performance air compression systems for manufacturing, automotive, construction, and industrial applications. V-shaped compressors, designed with cylinders arranged in a “V” configuration, offer superior balance, reduced vibration, and high volumetric...

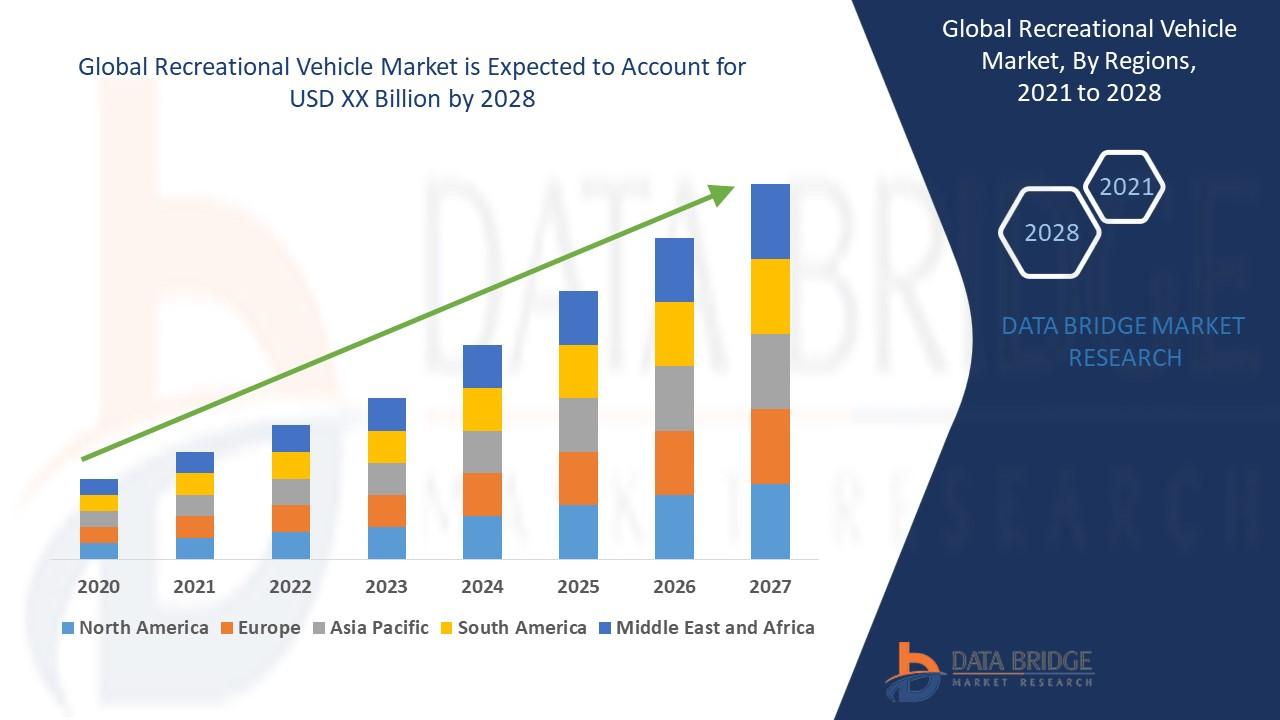

"Executive Summary Recreational Vehicle Market Research: Share and Size Intelligence CAGR Value The global recreational vehicle market size was valued at USD 69.09 billion in 2024 and is projected to reach USD 115.99 billion by 2032, with a CAGR of 6.69% during the forecast period of 2025 to 2032. The large scale Recreational Vehicle Market report gives explanation about...