Key Developments Influencing IT Security Worldwide

The United States public sector, encompassing federal, state, and local government agencies, represents a massive, complex, and strategically vital component of the overall It Security Market Share. This market segment is driven by a unique and powerful set of factors that differentiate it from the commercial market. First and foremost, government agencies at all levels are a high-value and constant target for a wide range of sophisticated cyber adversaries, from financially motivated ransomware gangs attacking local school districts to highly sophisticated, state-sponsored espionage groups targeting federal agencies for national secrets or to disrupt critical infrastructure. This creates a non-discretionary and mission-critical need for robust cybersecurity that is directly tied to national security. Second, the federal government, through a series of landmark executive orders and policy directives, has mandated a major, government-wide push to modernize its cybersecurity posture, with a very strong and explicit emphasis on adopting a "Zero Trust" architecture. This top-down, compliance-driven mandate from the highest levels of government is a powerful catalyst, driving significant and sustained spending on a new generation of security technologies across all federal agencies and the broader defense industrial base. The public sector is not just another vertical market; it is a central and strategic driver of the entire US cybersecurity industry.

Key Players

The key players serving the US public sector cybersecurity market are a specific and highly specialized ecosystem of companies. The first group consists of the major US defense and aerospace giants, like Lockheed Martin and Northrop Grumman. These companies have deep, long-standing relationships with the Department of Defense (DoD) and the intelligence community and are often the prime contractors on the largest and most sensitive security programs. The second group of key players are the major commercial cybersecurity vendors—such as Palo Alto Networks, Microsoft, CrowdStrike, and Zscaler—who have all made a major strategic and financial investment in building dedicated federal government sales teams and in getting their products through the rigorous government certification processes, such as FedRAMP for cloud services. Microsoft is a particularly strong key player in this space due to its massive, entrenched footprint across all levels of government. A third, and absolutely critical, group of players are the specialized government system integrators (SIs) and "beltway bandits." These firms, based largely around the Washington D.C. area, have deep expertise in navigating the complex federal procurement process and, crucially, provide the cleared personnel needed to work on sensitive and classified government projects. They are an essential channel to market for the technology vendors. The Cybersecurity and Infrastructure Security Agency (CISA) is also a key player, acting as the nation's primary civilian cyber defense agency and providing guidance and services to other federal agencies.

Future in "It Security Market Share"

The future of the US public sector cybersecurity market, and its contribution to the industry's growth rate, will be a story of the deep and wide implementation of Zero Trust architectures and a massive focus on securing the nation's critical infrastructure. The future will see a multi-year, government-wide effort to move away from the traditional network perimeter model and to fully implement a Zero Trust security framework, which will drive a sustained demand for modern Identity and Access Management (IAM), micro-segmentation, and Secure Access Service Edge (SASE) technologies. A second major future trend will be a much greater public-private partnership in the area of threat intelligence sharing and collective defense, particularly for the protection of the nation's 16 designated critical infrastructure sectors (such as energy, finance, and healthcare), a collaborative model that is a key feature of the US national security strategy. The future will also see a massive investment in securing the software supply chain for all software used by the government, driven by initiatives like the requirement for a "software bill of materials" (SBOM). The scale of the US government's IT and OT infrastructure makes its cybersecurity modernization a uniquely large and complex challenge compared to the public sector markets in any other region, including Europe or APAC.

Key Points "It Security Market Share"

This analysis highlights several crucial points about the US public sector cybersecurity market. The primary drivers are the high level of threat from state-sponsored actors and a strong, top-down federal mandate for cybersecurity modernization, particularly towards a Zero Trust model. The key players are a mix of the major defense contractors, the leading commercial cybersecurity vendors with dedicated federal teams, and the essential government system integrators. The future of the market's growth will be a long-term, multi-billion-dollar effort to implement Zero Trust across the entire federal government and to enhance the cybersecurity of the nation's critical infrastructure. The US public sector is not just a large market; it is a strategic and highly influential one that often sets the security standards and best practices that are later adopted by the private sector, contributing significantly to the overall worth and direction of the industry. The It Security Market Share is projected to grow to USD 495.62 Billion by 2035, exhibiting a CAGR of 11.37% during the forecast period 2025-2035.

Top Trending Reports -

Categorias

Leia mais

What’s Fueling Executive Summary Chickenpox Vaccine Market Size and Share Growth The global Chickenpox Vaccine market size was valued at USD 1.29 billion in 2024 and is projected to reach USD 1.78 billion by 2032, with a CAGR of 4.09% during the forecast period of 2025 to 2032. To stand apart from the competition, a careful idea about the competitive landscape, their product...

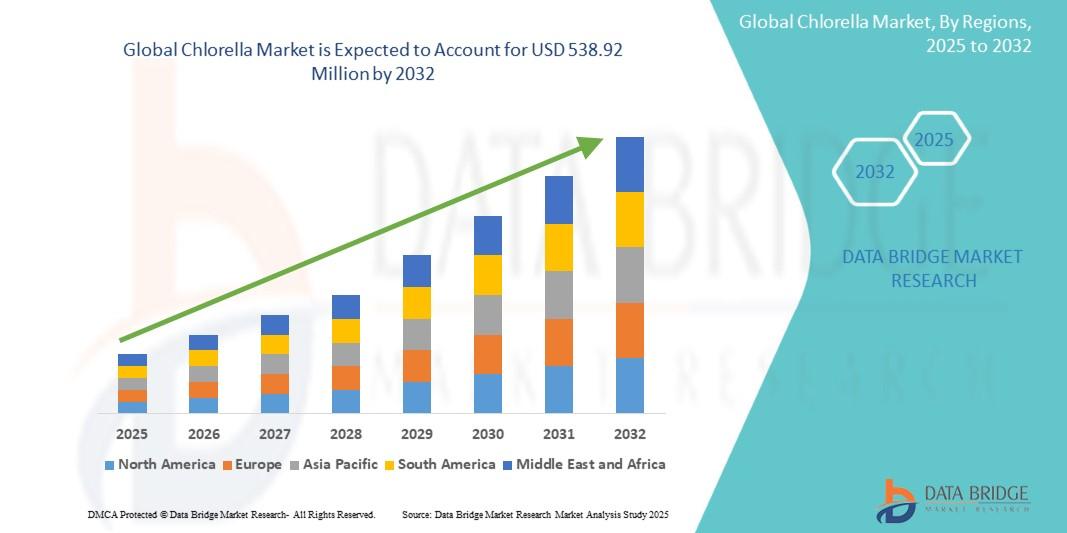

Introduction The Chlorella Market is experiencing rapid growth as the global demand for natural health supplements, superfoods, and sustainable nutrition solutions continues to rise. Chlorella, a nutrient-dense green microalgae, is renowned for its high protein content, vitamins, minerals, antioxidants, and detoxifying properties. It is widely used in dietary supplements, functional...

The Healthcare $\text{RFID}$ (Radio Frequency Identification) Market utilizes non-contact wireless technology to automatically identify and track tags attached to objects or people. In healthcare, $\text{RFID}$ is used to improve operational efficiency, enhance patient safety, and manage high-value assets.Healthcare RFID Market. The market is driven by the need for better inventory control and...

Latest Insights on Executive Summary Hearing Aids Market Share and Size The global hearing aids market size was valued at USD 9.79 billion in 2025 and is expected to reach USD 16.69 billion by 2033, at a CAGR of 6.90% during the forecast period. The market growth is largely fueled by the growing adoption of advanced healthcare technologies and the...

Executive Summary Reinforced Concrete Floor Market Opportunities by Size and Share The global reinforced concrete floor market was valued at USD 120.11 billion in 2024 and is expected to reach USD 184.33 billion by 2032 During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 5.5%, primarily driven by the increasing demand for sustainable, durable, and...