Liquid Embolic Market Analysis: U.S. Focus on Neurovascular Therapies and Endovascular Innovation

The Liquid Embolic Market is entering a compelling phase of evolution in the United States, driven by structural changes in neurovascular intervention, advanced device innovations, growing prevalence of intracranial aneurysms and arteriovenous malformations (AVMs), and a broader shift toward minimally invasive endovascular therapies. Liquid embolic agents—specialized biomaterials delivered via catheter to occlude abnormal blood vessels—play a critical role in treating complex vascular conditions such as cerebral aneurysms, AVMs, peripheral vascular malformations, and gastrointestinal bleeds. U.S. interventional radiology, neurosurgery and cardiovascular systems are increasingly relying on embolic technologies that offer precision, reduced procedural time, and improved patient outcomes. For a comprehensive overview, consult the Liquid Embolic Market analysis.

In the U.S., the migration from open surgical interventions to catheter-based solutions is accelerating. Endovascular therapy offers patients shorter hospital stays, faster recovery times, and fewer complications. Liquid embolic agents such as Onyx (ethylene vinyl alcohol copolymer), precipitating hydrophobic injectable liquid (PHIL), n-butyl cyanoacrylate (NBCA), and newer surface-modified polymer platforms are becoming essential tools in the neurointerventional toolkit. U.S. neurosurgeons and interventional radiologists are driving device adoption as they expand their portfolios of AVM and aneurysm treatments, especially in cases where coiling or stenting alone may not suffice. The Liquid Embolic Market is benefitting from expanded clinical guidelines, improved imaging (e.g., 3D rotational angiography, flat-panel CT), better catheter compatibility, and refined operator training programs, all of which enhance procedural success and broaden patient eligibility.

Looking ahead, the U.S. liquid embolic landscape presents ample opportunity, though it also faces significant challenges. Regulatory pathways, reimbursement considerations, hospital budget constraints, and competitive device pricing must be carefully navigated. Market players who can demonstrate clinical superiority, cost-effectiveness, ease of use, and compatibility with next-generation imaging and navigation platforms will be best positioned. As neurovascular and peripheral-vascular treatment volumes rise, and as population aging, lifestyle factors, and improved diagnostic screening increase demand, the Liquid Embolic Market in the U.S. is set for meaningful growth.

FAQs

1. What conditions drive liquid embolic use in the U.S.?

Intracranial aneurysms, arteriovenous malformations, gastrointestinal bleeds, peripheral vascular malformations and trauma-related vessel lesions.

2. Why is the market shifting toward liquid embolics?

They allow precise occlusion of abnormal vessels with minimally invasive catheter delivery, reducing surgical morbidity and hospital stay.

3. What must manufacturers focus on?

Clinical evidence, procedural ease, cost-effectiveness, reimbursement strategy and operator training.

Kategorien

Mehr lesen

Executive Summary Goat Cheese Market: Growth Trends and Share Breakdown The global goat cheese market size was valued at USD 11.32 billion in 2024 and is expected to reach USD 17.11 billion by 2032, at a CAGR of 5.30% during the forecast period The Goat Cheese Market report has been formed with the appropriate expertises that utilize established and unswerving...

Executive Summary: Woodworking Router Bits Market Size and Share by Application & Industry The global woodworking router bits market size was valued at USD 3.55 billion in 2024 and is projected to reach USD 5.27 billion by 2032, with a CAGR of 5.05% during the forecast period of 2025 to 2032. A worldwide Woodworking Router Bits Market report comprises of the most recent market...

The latest business intelligence report released by Polaris Market Research on Latex Agglutination Test Kits Market Share, Size, Trends, Industry Analysis Report, By Test Type (Antibody Detection, Antigen Testing, and Others); By Sample Type; By End User; By Region; Segment Forecast, 2024 – 2032. It covers the in-depth knowledge of the Latex Agglutination Test Kits Market...

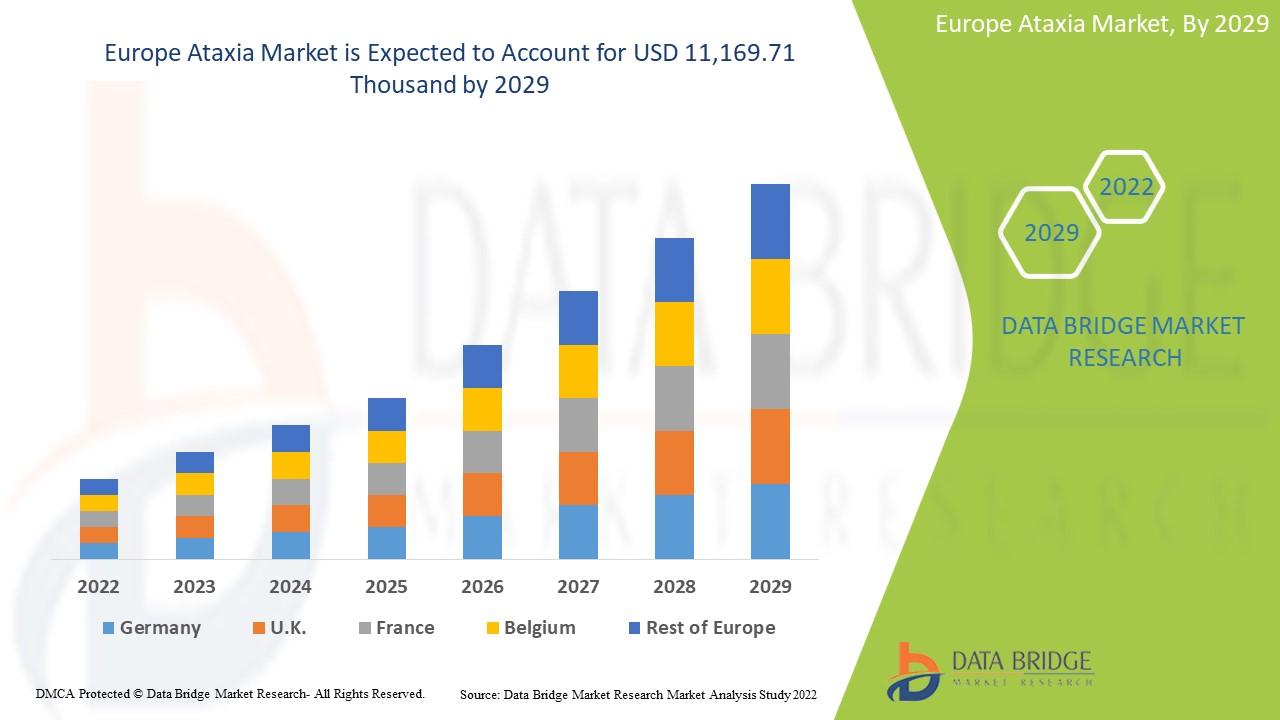

"Executive Summary Europe Ataxia Market Size and Share Forecast CAGR Value The Europe ataxia market is expected to gain market growth in the forecast period of 2022 to 2029. Data Bridge Market Research analyses that the market is growing with a CAGR of 5.8% in the forecast period of 2022 to 2029 and is expected to reach USD 11,169.71 thousand by 2029 from USD 7,424.22 thousand...

The Global Stye Drug Market size was valued at USD 8.16 Billion in 2024 and is expected to reach USD 9.83 Billion by 2032, at a CAGR of 5.20 % during the forecast period. The global business landscape is undergoing a transformation, with industries increasingly leaning on deep research and actionable insights to make strategic decisions. One segment seeing...