Taller, Stronger, Greener: The Next Chapter for APAC Wind Towers

Introduction

The APAC Wind Tower Market is expanding rapidly as Asia-Pacific accelerates wind power deployment to meet rising electricity demand, decarbonize grids, and enhance energy security. Wind towers—supporting nacelles, rotors, and control systems—are critical for turbine performance, influencing hub height, power capture, structural integrity, and lifecycle costs. As projects move onshore to higher hub heights and offshore into deeper waters, demand is shifting toward taller steel tubular towers, hybrid concrete–steel designs, prestressed concrete towers, and specialized offshore substructures such as monopiles, jackets, and floating platforms. Supply chains across China, India, Vietnam, South Korea, and Japan are scaling with new steelmaking capacity, heavy fabrication yards, and port upgrades. With governments setting ambitious renewable targets and local-content policies, the APAC wind tower market is poised for strong growth, driven by utility-scale onshore additions and a sharp ramp-up in offshore wind, including floating wind pilots transitioning to commercial arrays.

Market Drivers

Rising electricity demand, urbanization, and electrification across APAC are central drivers, pushing utilities toward low-carbon capacity additions. Policy support—auctions, feed-in premiums, renewable portfolio standards, and green finance—continues to expand onshore projects and unlock offshore zones. Taller towers (140–170 m hub height) enable improved capacity factors in suboptimal wind regimes common in parts of India and Southeast Asia, enhancing project bankability. Offshore wind buildouts in China, Taiwan, Japan, and South Korea stimulate demand for large-diameter monopiles, XL jackets, transition pieces, and corrosion-protected towers. Localization policies foster domestic tower manufacturing, lowering logistics costs and import risks. Advancements in high-strength steels, automated welding, nondestructive testing (NDT), and digital quality assurance improve tower reliability while reducing weight per MW.

Market Challenges

Volatility in steel plate prices and limited availability of large-diameter rolling capacity can squeeze manufacturer margins and disrupt bid assumptions. Heavy-lift logistics—from factory to site—face bottlenecks: bridge clearances, road curvature limits, and port crane availability. For offshore, competition for installation vessels and port marshalling space creates schedule risk. Quality deviations in welding, flange flatness, or coating can escalate rework and warranty exposure. Permitting complexity, social acceptance concerns, and grid interconnection queues may delay projects. Typhoon and seismic design requirements in parts of East Asia increase engineering complexity and cost. For floating wind, standardization, anchor supply, and serial fabrication remain early-stage, constraining near-term scale.

Market Opportunities

Hybrid and concrete segmental towers unlock higher hub heights without oversize road transport, ideal for mountainous or dense regions. Modularized tower sections and on-site assembly reduce logistics pain points. Offshore growth opens large opportunities in corrosion systems, thermal-sprayed aluminium (TSA) coatings, and advanced paint systems. Floating wind creates new value pools: steel or concrete floaters (semisubmersible, spar, barge), moorings, and dynamic cables—each requiring adapted tower-to-floater interfaces. Digitally enabled towers with embedded sensors (strain, vibration, corrosion potential) support structural health monitoring and life extension. Green steel and low-carbon cement adoption can differentiate bids in sustainability-focused tenders. Regional export platforms—e.g., Vietnam and India for onshore towers; South Korea and Japan for offshore substructures—can serve APAC and Middle East demand.

Regional Insights

China remains the largest wind market, with extensive onshore manufacturing and rapid offshore additions near coastal provinces. Domestic steel capacity, plate rolling lines, and fabrication yards give Chinese tower makers a cost and scale edge. India’s market is rebounding through auction-led pipelines and repowering, with growing interest in >140 m hybrid towers to unlock lower wind sites; ports on the west and east coasts are gearing for future offshore. Southeast Asia—Vietnam, the Philippines, and Thailand—pursues onshore corridors and early offshore pilots; Vietnam is emerging as a fabrication hub leveraging its coastline and skilled welders. Taiwan sustains a robust offshore supply chain with localization of towers, transition pieces, and jackets, feeding Round 3 projects. Japan and South Korea advance fixed-bottom and floating wind, supported by maritime industries and heavy fabrication; both are investing in specialized ports and serial production capability. Australia’s nascent offshore program complements strong onshore activity in VIC, NSW, and SA, with transmission buildouts shaping siting decisions.

Future Outlook

APAC wind tower demand will increasingly skew toward: (1) taller onshore towers using hybrid or concrete solutions to raise capacity factors; (2) offshore towers integrated with larger 15–20+ MW turbines, XL monopiles, and jackets; and (3) floating wind towers standardized for modular floater families. Expect faster adoption of robotic welding, AI-based NDT, and digital twins for fatigue life tracking and predictive maintenance. Sustainability pressure will accelerate green steel procurement and recyclable coating systems. As grid-forming inverters and hybrid wind-plus-storage proliferate, capacity factors and dispatchability will improve, supporting premium PPA pricing. Standardization and serial fabrication of offshore components—combined with port industrial clusters—should lower LCOE and smooth schedules by late decade.

Conclusion

The APAC Wind Tower Market stands at the center of the region’s renewable buildout. Policy momentum, rising hub heights, and the offshore surge—particularly in Northeast Asia—are expanding opportunities across steel plate supply, fabrication, logistics, and coatings. While steel volatility, logistics constraints, and coastal permitting remain hurdles, the shift to modular towers, digital QA, and localized industrial clusters is improving cost, quality, and schedule certainty. With continued investment in ports, heavy-lift assets, and workforce skills, APAC suppliers are positioned to scale onshore and offshore solutions, including floating wind. The result is a resilient, regionally anchored value chain capable of delivering reliable, low-cost wind energy at industrial scale.

الأقسام

إقرأ المزيد

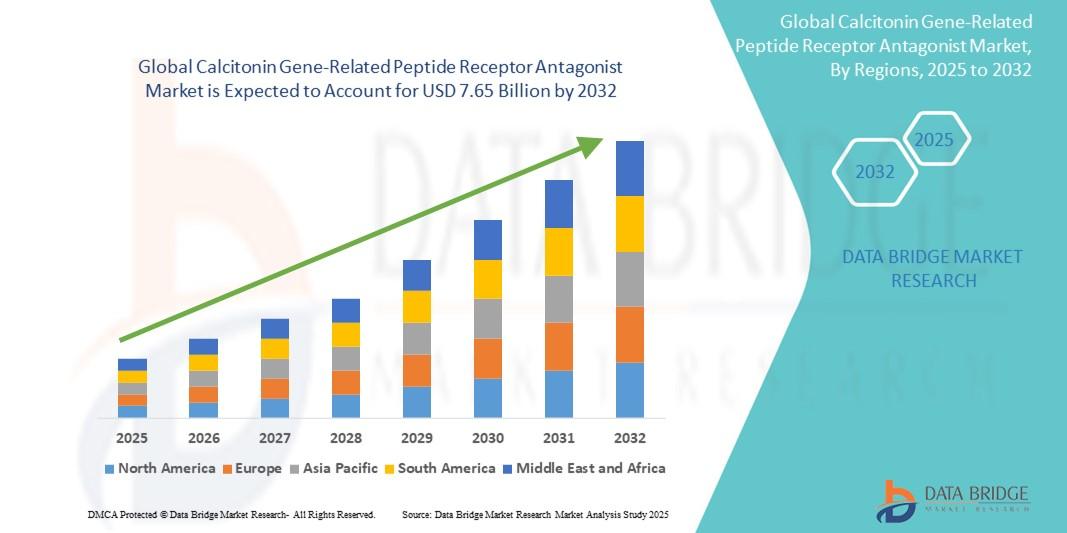

"Executive Summary Calcitonin Gene-Related Peptide Receptor Antagonist Market Size and Share Analysis Report CAGR Value The global calcitonin gene-related peptide receptor antagonist market size was valued at USD 3.38 billion in 2024 and is expected to reach USD 7.65 billion by 2032, at a CAGR of 10.73% during the forecast period Businesses are very much...

The global lice treatment market size was valued at USD 113.37 billion in 2024 and is expected to reach USD 189.76 billion by 2032, at a CAGR of 6.65% during the forecast period. The global business landscape is undergoing a transformation, with industries increasingly leaning on deep research and actionable insights to make strategic decisions. One segment seeing...

Executive Summary Optoelectronic Market: Growth Trends and Share Breakdown The optoelectronic market is expected to witness market growth at a rate of 13.92% in the forecast period of 2022 to 2029. While preparing this professional and exhaustive Optoelectronic Market research report, customer requirement has been kept into focus. Market type, size of the organization, availability...

The aerospace industry continues to drive technological advancement, linking transport, defense, and exploration with global development. With forecasted growth at a CAGR rate of 2.9% and forecasted market value of $51.6 Billion by 2031, the sector remains captivating for investment and talent. Of the sectors continually driving interest and strategic transformation, the Military Aviation...

"Competitive Analysis of Executive Summary Asia-Pacific Coordinate Measuring Machine Market Size and Share Data Bridge Market Research analyses that the coordinate measuring machine market will exhibit a CAGR of 9.00% for the forecast period of 2022-2029. Therefore, the coordinate measuring machine market value would rocket up to USD 1,825.49 by 2029. To stand apart from the...