Global MPLS Market Overview, Opportunities & Future Outlook | 2035

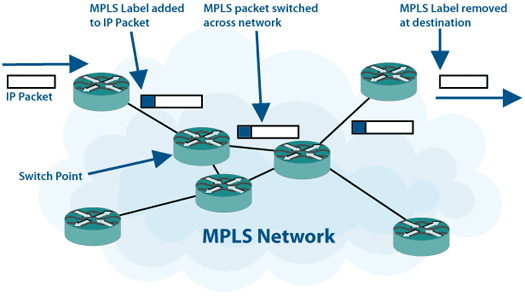

The contemporary Mpls Market Competition is defined by a single, powerful, and transformative rivalry: the battle between traditional, carrier-managed MPLS and the more modern, agile, and software-defined approach of SD-WAN. This is not just a competition between two technologies; it is a clash of two fundamentally different philosophies of wide area networking. MPLS represents the traditional, carrier-centric model, where the intelligence resides within the service provider's network. It is built on a foundation of reliability, security, and guaranteed performance, delivered via a private, dedicated network infrastructure. This makes it the gold standard for applications that require absolute predictability and have zero tolerance for performance degradation. However, this reliability comes at a high cost, long provisioning times, and a rigid architecture that is ill-suited for the dynamic, cloud-first world. The MPLS model often forces all traffic from branch offices, including cloud-bound traffic, to be "backhauled" through a central corporate data center for security inspection, an inefficient and high-latency process known as the "trombone effect."

In stark contrast, SD-WAN represents a decentralized, application-centric, and transport-agnostic model. It places the intelligence at the edge of the network, in a software-based controller and on-site appliances or virtual machines. The key competitive advantage of SD-WAN is its flexibility. It can use any available network transport—including MPLS, business broadband, and even 4G/5G wireless—and can be programmed to intelligently route different types of application traffic over the most appropriate path based on real-time network conditions and business policies. For example, it can send critical voice traffic over the reliable MPLS link while routing less-critical Microsoft 365 traffic over a lower-cost broadband connection with a direct internet breakout from the branch. This provides enormous benefits in terms of cost savings, agility (as new broadband circuits can be provisioned much faster than MPLS), and improved performance for cloud applications. This direct challenge to the MPLS value proposition has forced every enterprise and service provider to re-evaluate their WAN strategy.

The resolution of this intense competition is not the complete replacement of MPLS by SD-WAN, but rather the emergence of a new, integrated paradigm known as Secure Access Service Edge (SASE). The market is recognizing that the debate is no longer just about connectivity (MPLS vs. SD-WAN) but about the convergence of networking and security. SASE extends the principles of SD-WAN by integrating a full suite of cloud-delivered security services, such as a firewall-as-a-service (FWaaS), a secure web gateway (SWG), and zero-trust network access (ZTNA). This creates a single, unified architecture that can securely connect any user or device to any application, regardless of location. In this new competitive landscape, MPLS becomes one of several available "underlay" networks that the SASE architecture can leverage. The competition has therefore evolved. It is no longer a simple choice between MPLS and SD-WAN, but about which provider can offer the most comprehensive, secure, and easy-to-manage SASE solution that intelligently orchestrates traffic across a hybrid network of both private MPLS and public internet links. The Mpls Market size is projected to grow to USD 79.31 Billion by 2035, exhibiting a CAGR of 6.37% during the forecast period 2025-2035.

Top Trending Reports -

Corporate Game Based Learning Market

Categorias

Leia Mais

The steady and reliable Human Resource Outsourcing Market Growth is being driven by a powerful set of global business trends that are making the delegation of HR functions an increasingly attractive and strategic choice for companies of all sizes. The market's consistent upward momentum is clearly captured in forecasts that predict its valuation will reach USD 446.25 billion by 2035....

As Per Market Research Future, a detailed Woodworking Machine Market analysis reveals key insights into trends, challenges, and opportunities within the industry. The analysis highlights the increasing adoption of timber cutting and shaping equipment, as well as CNC wood processing systems, as major drivers of market dynamics. Challenges such as fluctuating raw material prices and skilled labor...

"Market Trends Shaping Executive Summary Europe Medical Devices Market Size and Share Medical devices market is expected to gain market growth in the forecast period of 2021 to 2028. Data Bridge Market Research analyses that the market is growing with a CAGR of 4.6% in the forecast period of 2021 to 2028 and is expected to reach USD 4,141.09 million by 2028 from USD 2,877.97 million...

Regional Overview of Executive Summary Europe Agricultural Lubricants Market by Size and Share Data Bridge Market Research analyses that the agricultural lubricants market was valued at USD 457.23 million in 2021 and is expected to reach the value of USD 645.27 million by 2029, at a CAGR of 4.4% during the forecast period. A study about the Europe Agricultural Lubricants Market...

Childhood is a time of discovery, imagination, and endless energy. Every parent wants their child to learn, grow, and stay active while having fun. Among all the toys and gadgets out there, few can match the lasting value of a Cycle for Kids. It’s more than just a fun activity—it’s a complete learning experience that helps children grow physically, mentally, and...