The Race for Dominance: Analyzing Mobility as a Service Market Share

The global contest for Mobility as a Service Market Share has ignited a fierce battle among a diverse set of companies, each aiming to become the default digital interface for urban transportation. The stakes are incredibly high, as market leadership could mean controlling the gateway to a sector projected to be worth over USD 754.341 billion by the year 2032. This market is expanding at a rapid clip, with forecasts showing a compound annual growth rate of 17.4%, which only intensifies the competition. In many cities, the dynamics lean towards a "winner-takes-most" scenario, where the platform with the most comprehensive service offering and the largest user base gains a nearly insurmountable advantage due to powerful network effects. This makes the early-stage race for market share a critical determinant of long-term success.

The players vying for market share come from various backgrounds, each with unique strengths and strategies. First are the pure-play MaaS aggregators, such as Whim or Trafi, who focus on building the technology platform and partnering with as many transport providers as possible. Their strength lies in their neutrality and their deep focus on the user experience. Competing directly with them are the established ride-hailing and delivery giants like Uber and Grab. These companies are leveraging their massive existing user bases and strong brand recognition to evolve into "super-apps," adding public transit, scooters, and other services to their core offering. They aim to dominate by becoming the one-stop-shop for all urban needs, not just transport.

Another critical group of contenders are the public transport authorities (PTAs) and municipal governments. Many PTAs are developing their own MaaS applications to ensure that public transit remains the backbone of urban mobility and to avoid ceding control of their transportation networks and valuable data to private, third-party companies. Their advantage is their direct control over the core transit system and their public service mandate. Finally, traditional automotive OEMs like Ford, BMW, and Toyota are investing heavily in mobility services. They see MaaS as a vital future revenue stream and are launching their own car-sharing, subscription, and MaaS platforms to capture a piece of the service-based mobility pie and maintain a direct relationship with consumers in a post-ownership world.

The strategies employed to capture and grow market share are multifaceted. Building the most comprehensive service portfolio is paramount; the platform with the most options is inherently more useful. Forming strategic partnerships with key transport operators, especially exclusive deals with public transit authorities, can be a major competitive advantage. Aggressive marketing and user acquisition tactics, including subsidies and promotional pricing, are often used to quickly build the critical mass needed to kickstart network effects. Offering compelling and flexible subscription models that lock in users and create recurring revenue is another key strategy. Ultimately, the winners will be those who can best navigate the complex web of partnerships, technology, and user needs to deliver the most reliable and convenient service.

Explore Our Latest Trending Reports:

Categorias

Leia Mais

Executive Summary Electronic Trial Master File (eTMF) Systems Market Opportunities by Size and Share The global electronic trial master file (eTMF) systems market size was valued at USD 1.84 billion in 2024 and is expected to reach USD 4.85 billion by 2032, at a CAGR of 12.90% during the forecast period An international Electronic Trial Master...

The Robotic Medical Imaging Market is evolving rapidly in the United States as advanced robotics combine with medical imaging platforms to drive precision diagnostics, workflow efficiency and remote-enabled care. Robotic systems integrated with imaging modalities—such as CT, MRI, ultrasound and PET/CT—are being deployed in U.S. hospitals, outpatient imaging centers and hybrid...

The respiratory-inhalers-market is experiencing robust growth, driven by the rising prevalence of respiratory diseases such as asthma and chronic obstructive pulmonary disease (COPD). With increasing awareness about non-invasive treatment options, patients and healthcare providers are increasingly adopting inhaler-based therapies. Technological advancements, such as smart inhalers with digital...

Hydraulic Fracturing Market Trends - Trends include the adoption of waterless fracking technologies, recycled water usage, digital well monitoring, and electric-powered fracking fleets (e-frac) for reducing emissions and costs. Current trends in the Hydraulic Fracturing Market are dominated by the pursuit of operational and capital efficiency. Trend 1: Intensity and Scale is paramount—the...

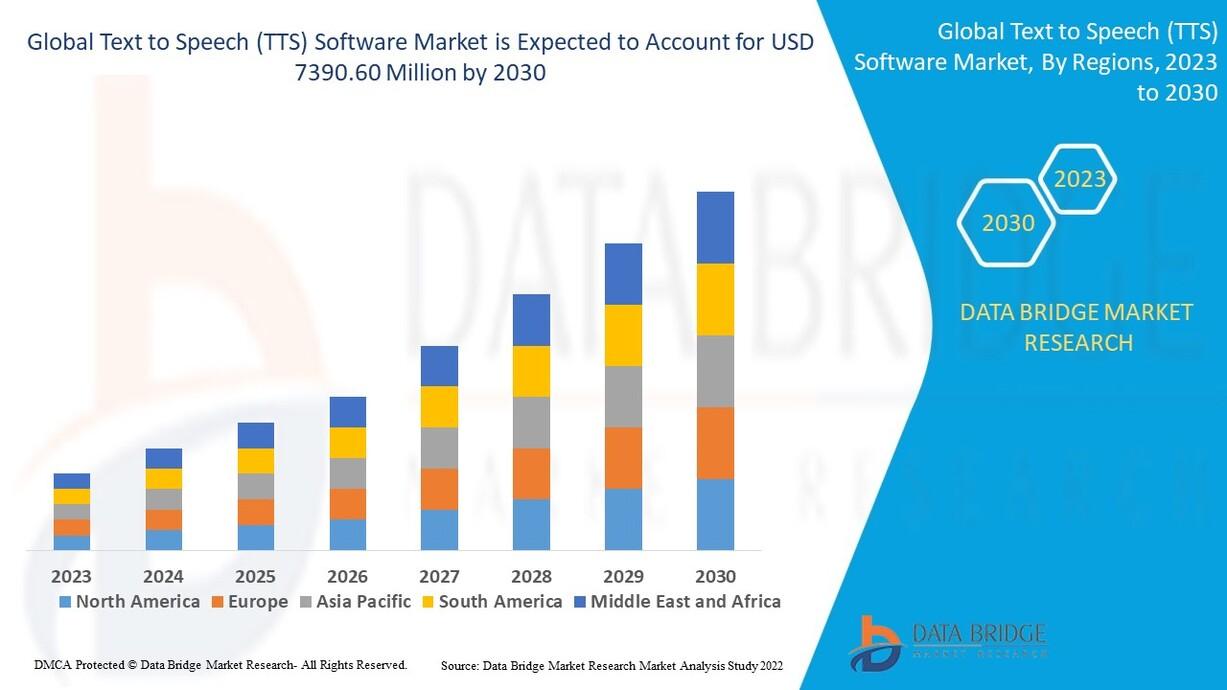

"Executive Summary Text to Speech (TTS) Software Market: Growth Trends and Share Breakdown CAGR Value Data Bridge Market Research analyses that the text to speech (TTS) software market is expected to reach USD 7390.60 million by 2030, which is USD 2285.66 million in 2022, registering a CAGR of 15.80% during the forecast period of 2023 to 2030. Being a premium market research report, Text...