The Rise of Smart Safety: Inside the US Collision Avoidance Market

Introduction

The US Automotive Collision Avoidance System Market is revolutionizing road safety by integrating intelligent technologies that detect and prevent potential crashes before they occur. As vehicle automation and advanced driver assistance systems (ADAS) evolve, collision avoidance systems have become a standard in modern automobiles. These systems use radar, camera, ultrasonic, and LIDAR sensors to monitor surroundings, warn drivers of potential hazards, and automatically apply brakes or adjust steering to avoid collisions. With the US witnessing rising vehicle ownership and road traffic, safety innovation is no longer optional — it’s essential. The market’s growth is being driven by regulatory mandates, consumer demand for safer vehicles, and rapid advances in sensor and AI-based systems.

Market Drivers

The primary driver for the US collision avoidance system market is the increasing emphasis on vehicle safety regulations by authorities such as the National Highway Traffic Safety Administration (NHTSA) and the Insurance Institute for Highway Safety (IIHS). Mandatory inclusion of features like automatic emergency braking (AEB) and lane departure warnings has accelerated market adoption. The rise in road accidents and driver distraction has pushed both OEMs and consumers to invest in proactive safety solutions. Technological advancements in radar and vision-based systems are making collision detection more accurate and affordable. Furthermore, the growing penetration of electric and connected vehicles in the US has created an ideal platform for integrating real-time, data-driven collision prevention systems.

Market Challenges

Despite rapid growth, the market faces several challenges. The high cost of advanced sensors and software integration makes collision avoidance systems expensive for lower-end vehicle segments. Sensor calibration errors and hardware malfunctions can affect reliability, especially under adverse weather conditions. Data processing and latency issues remain concerns for real-time decision-making in critical driving scenarios. Additionally, consumer overreliance on automation may lead to complacency, potentially undermining safety benefits. Manufacturers also face regulatory and ethical challenges in ensuring that automated systems make accurate split-second decisions in unpredictable environments. Supply chain disruptions in semiconductor components further add pressure to OEMs and Tier-1 suppliers.

Market Opportunities

Opportunities in the US collision avoidance system market are vast, particularly in AI integration and sensor fusion technology. Combining radar, camera, and LIDAR data into unified decision-making systems enhances accuracy and reliability. There is also a growing opportunity in the aftermarket segment as older vehicles undergo retrofitting with collision warning and braking systems. Expansion of vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication technologies promises new avenues for predictive collision avoidance. The commercial vehicle segment, including trucks and delivery fleets, is another major growth area as logistics operators prioritize driver safety and insurance benefits. Furthermore, strategic partnerships between automotive OEMs and software developers are expected to accelerate the development of cost-effective and scalable safety solutions.

Regional Insights

Regionally, automotive technology hubs such as California, Michigan, and Texas lead the adoption of collision avoidance systems in the US. California, home to major EV and autonomous driving innovators, drives software and AI advancements. Michigan remains a core manufacturing base for ADAS and sensor development, while Texas is witnessing growth in commercial vehicle integration. The Northeast region, particularly New York and Massachusetts, showcases strong consumer adoption due to urban traffic density and stringent safety awareness. The Midwest continues to dominate OEM and component production, supporting nationwide distribution. Overall, the US market benefits from a balanced ecosystem of manufacturing, research, and innovation centers driving technology adoption.

Future Outlook

The future of the US collision avoidance system market is deeply tied to the progression of autonomous and connected vehicle technologies. By 2035, most vehicles on American roads are expected to feature multi-layered safety architectures capable of predicting and avoiding accidents in real time. Artificial intelligence will enhance predictive capabilities, while 5G connectivity will enable faster data exchange between vehicles and infrastructure. The rise of fully autonomous vehicles will push the demand for redundant, fail-safe safety systems. Additionally, government initiatives promoting zero fatalities under “Vision Zero” programs will continue to support policy-driven adoption. As costs decline and mass production increases, collision avoidance systems will soon become standard across all vehicle classes.

Conclusion

In conclusion, the US automotive collision avoidance system market is at the forefront of redefining road safety through intelligence and automation. While high costs and technical integration remain hurdles, continuous advancements in AI, sensor accuracy, and communication networks are rapidly overcoming these barriers. The future of automotive safety lies in predictive and interconnected systems capable of responding faster than human reflexes. As the US moves toward a safer, smarter mobility ecosystem, collision avoidance technology will stand as one of the most significant pillars in achieving accident-free transportation.

Categories

Read More

IntroductionThe US Micro Battery Market is witnessing rapid expansion, driven by the surge in compact, portable, and smart electronic devices. These miniature power sources are essential for wearable electronics, medical implants, IoT sensors, and wireless communication devices. As consumer demand shifts toward smaller, lighter, and longer-lasting technologies, micro batteries are becoming...

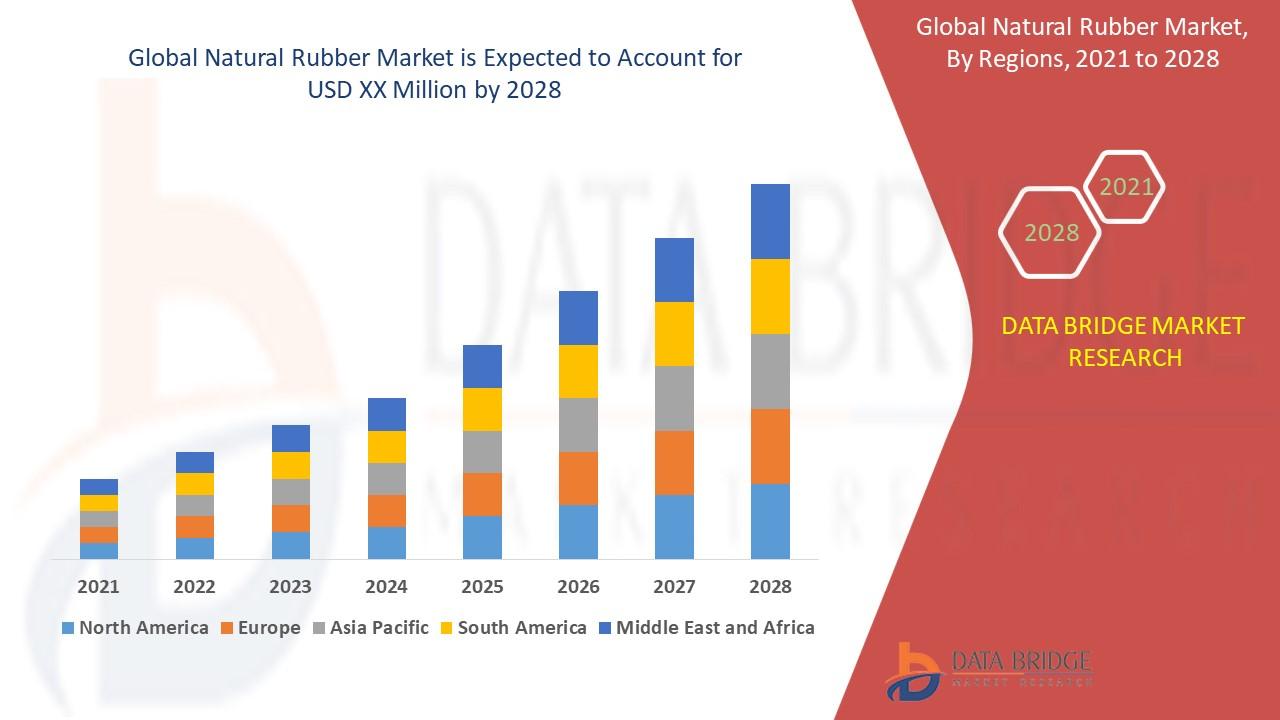

"In-Depth Study on Executive Summary Natural Rubber Market Size and Share CAGR Value The global natural rubber market size was valued at USD 18.30 billion in 2024 and is projected to reach USD 26.12 billion by 2032, with a CAGR of 4.55 % during the forecast period of 2025 to 2032. Natural Rubber Market research report contains a key data about the market, emerging trends,...

Keeping your home clean is not just about tidying up—it’s about maintaining a space where you feel comfortable, relaxed, and at peace. In Queen Creek AZ, house cleaning is a service that allows homeowners to enjoy a fresh, spotless environment without the stress of doing it themselves. Whether you’re busy with work, family, or other commitments, professional house cleaning...

Key Drivers Impacting Executive Summary Sauces, Dressings and Condiments Market Size and Share CAGR Value The sauces, dressings and condiments market is expected to gain market growth in the forecast period of 2023 to 2030. Data Bridge Market Research analyses the market is expected to reach USD 19.00 billion by 2030 from 10.58 billion in 2022 growing at a CAGR of 7.6 % during the...

Regional Overview of Executive Summary Umami Flavours Market by Size and Share The global umami flavours market size was valued at USD 1.16 billion in 2024 and is projected to reach USD 1.95 billion by 2032, with a CAGR of 6.70% during the forecast period of 2025 to 2032. With the superior Umami Flavours Market report, get knowledge about the industry which explains what market...